What is a Good Cap Rate for Multifamily?

Cap rates are a fundamental metric for return and value in commercial real estate investing across the board. For example, they tell us what yield real estate investors are willing to accept when they purchase an apartment community. Today Cap rates are continuing to compress as investors see cash-flowing hard assets as a low-risk way to store and grow value and achieve a solid cash-on-cash return.

In this guide, we’ll go into what is a good Cap rate for multifamily, what drives Cap rates in multifamily, how investors can force value, and how government bonds fit into the equation.

Key Takeaways

-

The capitalization rate is the return calculated on the property’s anticipated income. To find the property’s cap rate, you would divide the net operating income by the market value.

-

The pro forma CAP rate is very similar to calculating the in-place CAP rate; the only difference is that for the pro forma CAP rate, you would also include the renovation cost.

-

Cap rates vary from market to market across the United States and vary depending on the micro-location and condition of the investment property. Markets can be classified into three buckets: primary, secondary, and tertiary.

-

Cap rates also showcase the relationship between risk and return; a “low” cap rate of 3-5% would mean the asset is lower risk and higher value, while a “higher” cap rate of 8-10% reflects a lower price, meaning higher risk and a higher return.

What is the Net Operating Income (NOI)?

The NOI is your gross rental income – operating expenses. You may improve your property’s net operating income by lowering costs, making operational improvements, and charging more to collect more significant gross revenue. The higher your net operating income, the greater the value is, as a real estate investor would be prepared to pay more.

(Gross Income – Operating Expenses= NOI)

For example, if you collected $100,000 in monthly rent and had $40,000 in operating costs, that would leave you with $60,000 of NOI. As a result, that would mean you would have an annual NOI of $720,000 ($60,000 NOI X 12 Months= $720,000 NOI).

What is the Capitalization Rate (CAP)?

The capitalization rate is the return calculated on the property’s anticipated income. To find the property’s cap rate, you would divide the net operating income by the market value.

The relationship between CAP rates and multifamily valuations is inverse, which means that the higher the CAP rate, the lower the valuation is, and the lower the CAP rate, the higher the valuation is.

Cap rate calculation

(NOI / Current Market Value= Cap Rate)

For example; Let’s assume an apartment with a $720,000 NOI and a market CAP rate of 7%, giving it a value of $10,285,714 ($720,000 / 0.07 = Market Value).

Let’s assume there’s another apartment with a $720,000 NOI but a market CAP rate of 5%, giving it a value of $14,400,000 ($720,000 / 0.05= Market Value).

As you can see from the two scenarios above, the same $720,000 of NOI but a market CAP rate difference of 2% resulted in a net increase of $4,114,286 in valuation.

Pro forma cap rate

The pro forma CAP rate is very similar to calculating the in-place CAP rate; the only difference is that for the pro forma CAP rate, you would also include the renovation cost.

For example, Let’s assume that we make $2,500,000 in renovations on a multi-family property that we purchased for $10,285,714; our total cost would be $12,875,714. Once we stabilize the property/complete the renovation, the building will now produce $1,100,000 in NOI instead of $720,000 in NOI as in the previous example. This means that our proforma CAP rate is 8.5% ($1,000,000 / $12,875,714 = 0.085).

As you can see, there is a delta of 1.5% between the in-place CAP rate at 7% and the pro forma CAP rate at 8.5%. This tells us that after we perform the renovations, we will increase the return on capital as the building will produce a higher yield from cash flow post-renovations.

Whats a good CAP rate? | Market cap rates and valuation multiples

The value add strategy in multifamily is driven by finding ways to increase the NOI (Income – Expenses= NOI), and the formula to create that value is NOI / Market Cap= Valuation.

Below are examples of what every $1 of NOI would add in valuation to a multifamily community in a 4%, 5%, 6%, and 7% Cap market.

4% Cap Market – (1/ 0.04= $25) | Every $1 in NOI increase, adds $25 in valuation to the building in a 4% Cap market.

5% Cap Market – (1/ 0.05= $20) | Every $1 in NOI increase, adds $20 in valuation to the building in a 5% Cap market.

6% Cap Market – (1/ 0.06= $16) | Every $1 in NOI increase, adds $16 in valuation to the building in a 6% Cap market.

7% Cap Market – (1/ 0.07= $14) | Every $1 in NOI increase, adds $14 in valuation to the building in a 7% Cap market.

Components to a cap rate on an investment property

Location plays a profound impact in property cap rates. The price of land that settles in a hot and in-demand center is likely higher than that of a smaller community in a rural area.

Many factors dictate how Cap rates in apartments are priced, which is essentially a function of the risk premium associated with a given property and market. An excellent way to look at what risk premium is, for example, is, let’s say you can get a 2% yield on purchasing a very low-risk fixed U.S. government bond. But instead, you buy a 6% Cap multifamily property, which means that you are willing to take on more risk to seek 4% more yield than a virtually risk-free bond from the U.S. government.

That extra risk that a real estate investor takes to seek a higher yield is made of factors such as the following.

- Creditworthiness of tenant

- Tenant job diversification

- Local demographics

- Local economic drivers

- Supply and demand for the local market

- Age of the property

- Deferred maintenance (repairs needed)

- In-place rents vs. market rents

- And much more!

What higher caps and lower caps tell real estate investors about a property and market

Cap rates also showcase the relationship between risk and return; a “low” cap rate of 3-5% would mean the asset is lower risk and higher value, while a “higher” cap rate of 8-10% reflects a lower price, meaning higher risk and a higher return. Cap rates also help us understand what the purchase price of an asset could be if we know the NOI and what Cap rate the deal is being sold on.

Cap rates for different markets

Cap rates vary from market to market across the United States and vary depending on the micro-location and condition of the investment property. Markets can be classified into three buckets: primary, secondary, and tertiary.

1.) Primary Markets

Gateway markets are often referred to as primary real estate markets, the largest markets in the United States for housing. With over 5 million people, these cities are densely packed. They are financial hubs that include long-standing trade and extensive infrastructure and receive significant investment from the more prominent institutions. The strong economic drivers in these locations have resulted in the lowest CAP rates or returns compared to secondary and tertiary markets. This is mainly owing to their powerful economic engines. Real estate investing in one of these markets is quite a low risk due to the high activity level.

Primary markets Cap rates could be between 3% to 4.75% and include large cities like…

- San Francisco

- New York

- Los Angeles

- DC

- Chicago

- Boston

2.) Secondary Markets

Secondary real estate markets have many of the same features as primary markets, except that they are less densely populated, ranging from 1 to 5 million people. However, these markets are often quite large even though they aren’t as big as a primary market; they have significant population and economic growth.

Secondary markets Cap rates could be between 4% to 5.25% and include cities like…

- Miami

- Orlando

- Seattle

- Austin

- Charlotte

- And more

3.) Tertiary Markets

Tertiary real estate markets are also known as developing economies gaining ground. They’re less densely inhabited, with under 1 million individuals, and much more widely separated than typical primary and secondary markets. Tertiary markets generally have the highest CAP rates or yield compared to primary and secondary markets. It’s also important to note that tertiary markets tend to lag the faster CAP compression larger markets have.

Tertiary markets Cap rates could be between 5% to 7% and include cities like…

- Charleston

- Las Vegas

- Richmond

- Nashville

- And more

Multifamily cap rates: Good caps for multifamily

As previously discussed, Cap rates indicate the risk and return profile in a deal; therefore, your particular investment goals will determine the type of yield or Cap rates you seek to acquire. Here at Willowdale Equity, a good going in Cap rate for what fits the box for our investors and us is anywhere from a 5% to 7% Cap. This Cap rate range represents multifamily assets, in stable cash-flowing growth markets, with some renovation dollars that need to be implemented to make repairs and take the rental property to the next level.

Frequently Asked Questions About Multifamily Cap Rates 2024

A 7.5% cap rate means that if you were to purchase a real estate property all cash, you would be able to make a return of 7.5% from the cash flow that the property produces annually. This means that you would have less cash invested in a given deal, which produces a higher rate of return than what the cap rate suggests. It’s important to note that in commercial real estate, most purchases utilize debt.

What a “good cap rate” varies across asset classes and many other factors. But in general, if you can purchase a multifamily property at a 4%-6% cap, that would be a solid in-place rate of return with tons of room to upside cashflow potential.

A 4% cap is a solid capitalization rate in many major markets across the United States. It’s important to note that a lower cap rate like 4% represents the asset’s low level of risk, which as a result, means that cap rates are relative to the type of asset, location, and specific market that you’re buying.

Multifamily cap rates are so low because investors have a solid outlook on the multifamily asset classes’ performance for years to come. Therefore they are willing to pay more for these assets because they believe overall demand and rental income will continue to grow. Apart from the equation, also driving these buying behaviors are low-interest rates and high inflation.

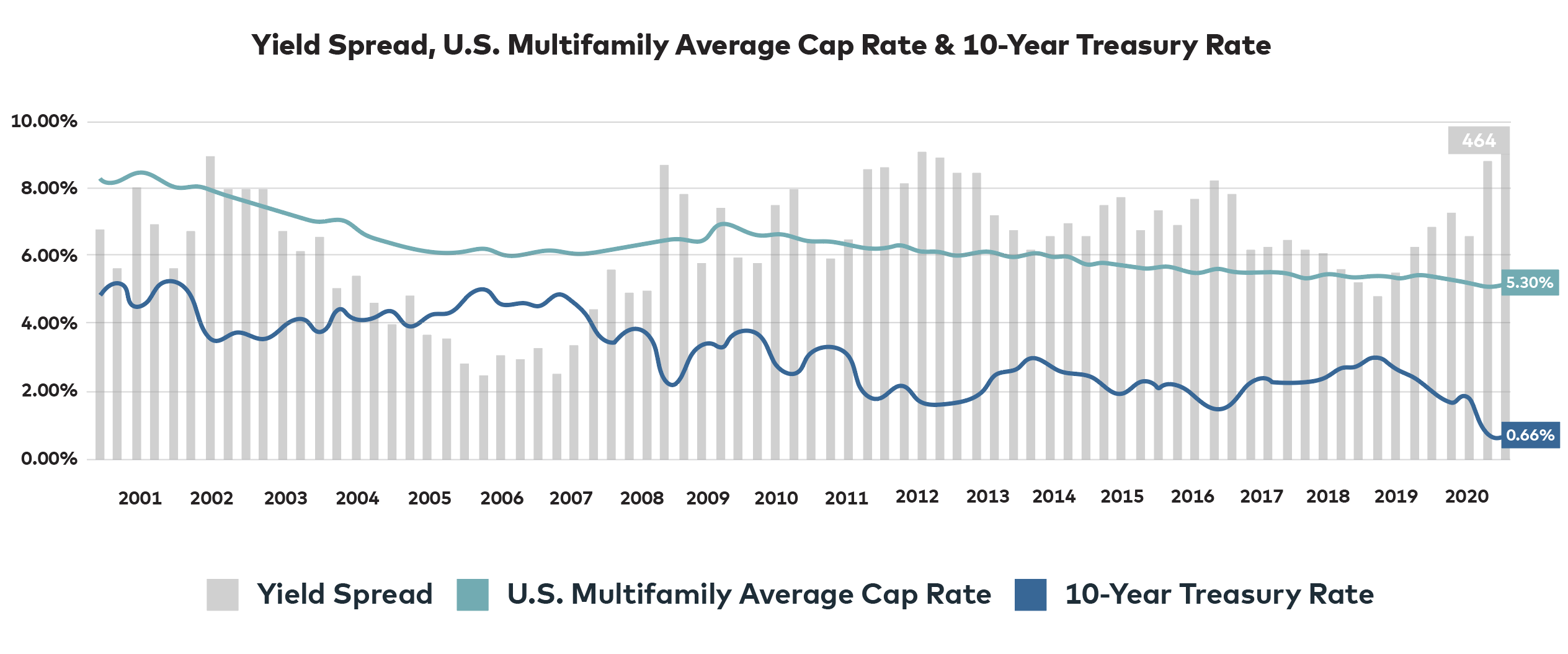

The 10 year treasury and cap rates

It’s just a ten-year debt obligation issued by the United States government with an expiration date of ten years. So you’re essentially loaning money to the United States government and receiving a predetermined interest rate on the cash every six months. The United States government also makes these loans available in 2, 3, 5, and 7-year terms with a greater yield on the 10-year note. The United States government is a secure investment vehicle since they are unlikely to default on a loan. In exchange for its security, investors receive a lower yield/rate of return.

Multifamily housing, often known as rentals or apartments, has outperformed other commercial real estates asset classes such as student housing, office, retail, and hotels in the long term.

Multifamily real estate’s value is determined by how much a real estate investor is prepared to accept as the yield on their purchase, based on current and future Net Operating Income (NOI).

The larger the spread, the stronger the outlook. As you can see above in late 2020-early 2021, there is a large spread in yields when looking back over the last decades.

You’ve discovered how value is calculated and how when CAP rates compress, it results in a greater value for each dollar of NOI. Now let’s compare it to the 10-year Treasury to understand where things are moving.

A 2-4 percent spread previously existed between CAP rates and 10-year Treasury yields, although this has narrowed recently. The higher yield spread measures the additional risk in a real estate investment relative to a super-low-risk investment like a government-issued bond. Multifamily and commercial property does not have an upper limit on returns, as bonds with fixed interest rates would.

When cash inflows and rents in residential and commercial real estate grow yearly, especially in an inflationary market, investors will sometimes purchase a property at a lower CAP rate. If analysts predict NOI to continue to grow, cap rates and 10-year Treasury yields will further spread from each other.

This is why the 10-year Treasury is an excellent barometer of investor sentiment towards the future value of commercial real estate investments.

Sources:

- Investopedia, “10-Year Treasury Note“

- Investopedia, “Understanding Treasury Yields and Interest Rates“

- CNBC, “U.S. 10 Year Treasury“

Interested In Learning More About PASSIVE Real Estate Investing In Multifamily Properties?

Get Access to the FREE 5 Day PASSIVE Real Estate Investing Crash Course.

In this video crash course, you’ll learn everything you need to know from A to Z

about passive investing in multifamily real estate.

We’ll cover topics like earned income vs passive income, the tax advantages, why multifamily, inflation, how syndications work, and much much more!