Capital Stack: Understanding The Commercial Real Estate Capital Stack

This article is part of our passive investors guide on real estate syndications, available here.

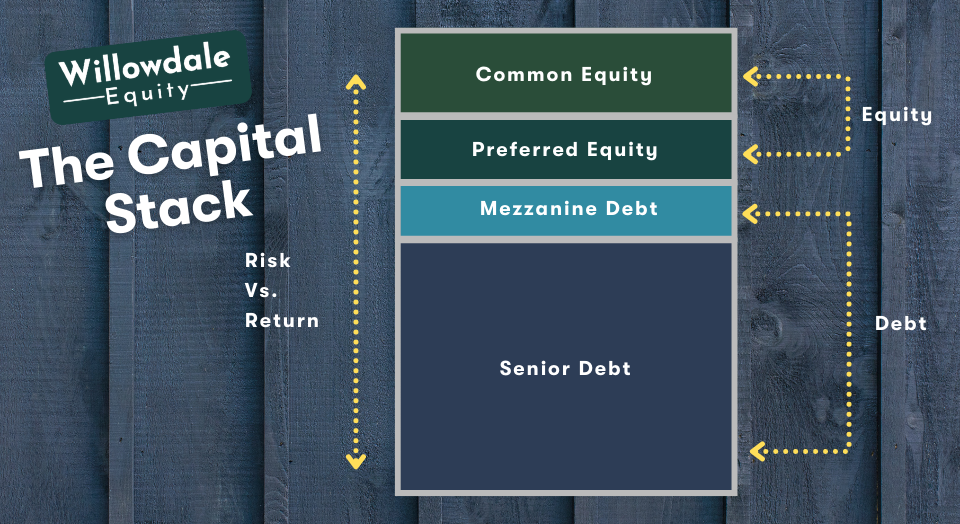

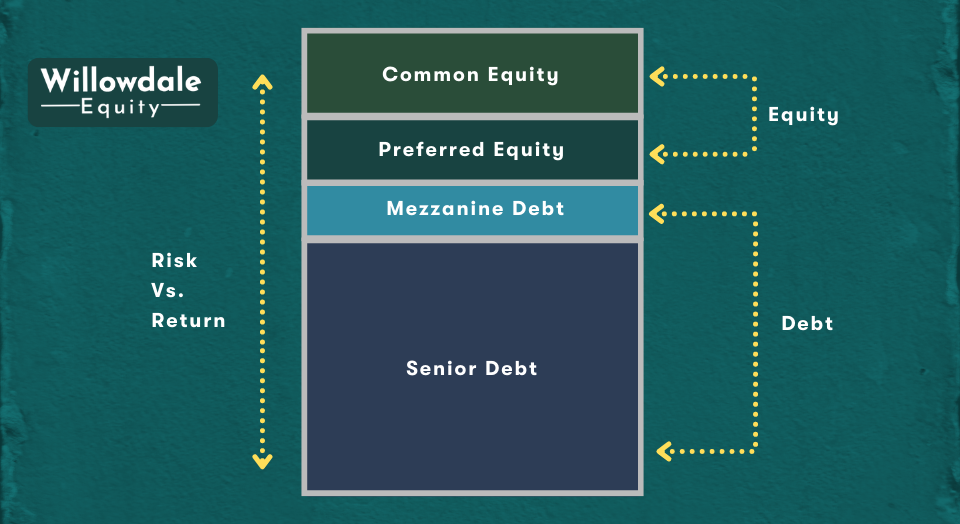

Real Estate Capital Stack

Each commercial real estate transaction has its own set of requirements. The capital structure for every multifamily deal will be different depending on that deal’s risk profile, return expectations, the specific plan for the deal, and any other specific needs the deal has. Investors are always asking, “why the capital structure is important?” and the simple answer to that is how you structure the capital to acquire a property will dictate the risk and return levels of the deal. The capital stack is a set of all the financial resources needed to finance a transaction, including internal and external funds.

A commercial real estate investment’s capital structure can be split into debt and equity. Suppose you’re a passive investor/limited partner in a multifamily real estate syndication. In that case, you’ll most likely invest your money in the equity pool, either as common equity or preferred equity in the project.

It’s also worth noting that leverage is essential to real estate investment returns. The lower the capital put into a transaction, the greater the return on that money. Once you understand this concept, you’ll see why multifamily syndication, for example, takes a variety of debt and leverage and is rarely financed with half equity and half senior debt.

Key Takeaways

-

When structuring real estate deals, how you structure capital will dictate how much risk there is in that deal and what return you can expect from your investment.

-

Senior debt is your first mortgage and is located at the very bottom of the capital stack, which makes it the lowest risk position in the capital structure.

-

Most investors will make a common equity investment or be preferred equity holders in a deal.

-

Equity investors sit at the very top of the capital structure and are regarded as the highest risk position compared to senior debt and mezzanine debt holders. Therefore both common equity holders and preferred equity shareholders receive the highest rate of return for their risk.

Capital stack diagram

Senior Debt

Senior debt is your first mortgage and is located at the very bottom of the capital stack, which makes it the lowest risk position in the capital structure. Senior debt is typically the largest investor in a commercial real estate deal. It’s referred to as senior, as it sits in a position senior to all the capital above it in the stack. Senior debt investors/senior debt holders receive returns on the lowest end of the capital stack as they have the lowest risk.

Every month, senior debt collects their contracted payment which includes interest or not, depending on the terms of the debt. This debt is secured through a lien on the property and is the first to be paid out in the event of a sale or foreclosure.

For Example, If the property defaults for failing to make its mortgage payments on the bank loan, the lender can seize the property via foreclosure.

Mezzanine Debt

Mezzanine debt sits right between the senior debt and the preferred or common equity position. Like senior debt, mezzanine debt investors receive monthly interest payments. They will generally receive a higher rate of return than senior debt as they sit subordinate to them with more risk.

Mezzanine debt lenders will receive security either through a junior lien on the property or through a pledge in shares from the equity offering in the deal. It’s important to note that the senior debt lender must approve having the mezzanine lender be a part of the deal. The senior debt and the mezzanine debt will enter into what is referred to as an intercreditor agreement which refers to who takes what in the event of default on the property. Generally, mezzanine debt is shorter-term and more expensive in commercial real estate. Therefore investors should have a clear exit strategy to take them out within the first few years of the project.

One important thing to keep in mind when considering mezzanine debt is you need to have a clear exit strategy to cash this piece of the capital stack out. Also, it should only be used as a last resort after all other funding options have been exhausted. The reason for this is that mezzanine debt typically comes with much higher interest rates and fees when compared to traditional financing products.

Related Read: Multifamily Recapitalizations: What to Look out for

Common Equity and Preferred Equity Investors

Equity investors sit at the very top of the capital structure and are regarded as the highest risk position compared to senior debt and mezzanine debt holders. Therefore both common equity holders and preferred equity shareholders receive the highest rate of return for their risk.

Preferred equity is like a hybrid of debt and equity and has some similarities to mezzanine debt as they receive their fixed payments monthly or quarterly, but generally, they don’t participate in the upside of equity built through the course of the deal. They also don’t have the same security that senior debt and mezzanine debt has, so as a result, they receive a higher rate of return on their capital.

Common equity is the position in the capital stack where real estate investors have the most opportunity to gain, as there is no ceiling on their returns. Equity investors are not guaranteed payments, even though they will likely receive monthly or quarterly distributions out of cash flows.

Common equity investors benefit and share in all the equity created through forced appreciation, market appreciation, and amortization. The two most common ways they will get to share in the equity gain would be through a refinance or the sale/disposition of the property. Equity capital is one of the most essential pieces of the capital stack due to the simple fact that most groups raise funds from multiple individual private investors.

Capital stack example

Let’s assume that we’re looking to purchase a 150-unit garden-style multi-family community in Atlanta, GA, and it costs us $10 million to buy this property.

To fund the total capitalization of the property, we could obtain a first mortgage of 75% LTV on the $10,000,000 purchase value, which would be a $7,500,000 loan.

Now we must raise equity to make up for the difference between the purchase price and the debt; in this case, about $2.5 million or 25% of the purchase price would need to be raised. Closing costs, prepaid reserves that the senior debt lender demands on closing, cash reserves, an acquisition fee, and much more are just a few of the expenses involved with the transaction. So we’ll have to raise an additional 5% equity, which would require us to now raise about $3 million or 30% of the $10 million purchase price.

For this example, let’s say that the passive investors/limited partners invest $1,500,000 in common equity and $1,500,000 in preferred equity. The return projections for both common and preferred equity will vary. This is why some investors like to diversify their capital contribution in the deal by investing in both positions to blend their risk profile in the investment.

Related Read: The Real Estate Waterfall Equity Structure

Frequently Asked Questions About The Commercial Real Estate Capital Stack

Equity in commercial real estate is what individual investors get for investing capital into a deal. Equity is a form of security for investors. In a commercial real estate deal, equity represents the amount left over after subtracting the property’s debt from the property’s current market value.

Real estate ground-up development deals tend to have more complex capital structures. This is due to the higher risk profile of building a property from scratch, limiting your ability to get affordable capital or all the capital you need from one or two sources. Real estate developers will often get creative with their capital structure to spread out the risk for investors to get to total capitalization.

The real estate developers’ equity sits in the same position as a limited partner (LP) common equity shareholder in a real estate deal.

Capital Stack - Conclusion

The capital stack is a set of all the financial resources needed to finance a transaction, including internal and external funds.

Most investors will make a common equity investment or be preferred equity holders in a deal. If you believe in the sponsor, and the project, the highest position in the stack would offer the highest returns but also pose the highest risk. This is where you have the most substantial opportunity to double your capital every 5-7 years. First, understand your risk tolerance, and then make the investment congruent with that to build a resilient investment portfolio.

Interested In Learning More About PASSIVE Real Estate Investing In Multifamily Properties?

Get Access to the FREE 5 Day PASSIVE Real Estate Investing Crash Course.

In this video crash course, you’ll learn everything you need to know from A to Z

about passive investing in multifamily real estate.

We’ll cover topics like earned income vs passive income, the tax advantages, why multifamily, inflation, how syndications work, and much much more!