Table of Contents

- What is a Schedule K-1 Form & How Does it Affect Your taxable income?

- Schedule K-1 Form Sections You Should Know

- When should I receive my K-1?

- Is rental income passive income?

- K-1 net rental real estate income

- How is K-1 income taxed and the passive income tax rate

- Business income, ordinary income for the tax professional. What you need to do with a Schedule K-1

- How does K-1 loss affect my taxes?

- The Tax Implications of Different Structures:

- The Consequences of Filing Extensions

- Frequently Asked Questions About How Does a K1 Affect My Personal Taxes

- How Is K1 Income Taxed - Conclusion

Every passive LP in a multifamily syndication confronts the same question come tax season: how is K-1 income taxed, and why does the number on the K-1 look almost nothing like the cash distributions that hit my account during the year? The short answer is that K-1 income is taxed at the LP's marginal rate as passive income — but the K-1 figure is a calculated net number, not the cash flow itself, and the gap between the two is where depreciation does its work.

The Schedule K-1 is the document the partnership files with the IRS (alongside its 1065 partnership return) to report each partner's share of the entity's income, deductions, credits, and distributions. For an LP in a typical Class B/C value-add multifamily deal, the most common pattern in the first few years of a hold is Box 2 (net rental real estate income) showing a paper loss while Box 19 (distributions) shows positive cash received. The two numbers are not contradictory — they're reporting different things.

This pillar walks through the form box by box, explains how passive K-1 income is actually taxed at the personal-return level, covers when LPs should expect to receive their K-1, and lays out the entity-type variations (partnership, S-corp, C-corp, trust, LLC) and the consequences of filing extensions. The goal is a working LP-level understanding of the form — not tax advice. Specific situations go to your CPA.

Key Takeaways

- The Schedule K-1 is how a multifamily syndication reports your share of the partnership's income, deductions, credits, and distributions to the IRS. The partnership itself doesn't pay tax — each LP pays the personal-level tax on their pro-rata share.

- The four K-1 boxes every LP needs to read: Box J (your ownership %), Box 2 (your net rental income or paper loss after depreciation), Box 19 (cash distributions you actually received), Box L (running capital account analysis).

- Box 2 frequently shows a paper loss while Box 19 shows positive cash distributions — that's depreciation passing through. The "loss" is non-cash and doesn't mean the deal underperformed; it's the tax shield that makes leveraged multifamily syndication efficient.

- K-1 passive losses normally offset only other passive income, not W-2 active income. The exception: real estate professional status (REPS), which can allow active-income offset if a household member spends 750+ hours per year materially participating in real estate.

- LPs should expect K-1s in mid-to-late March. Partnership returns (Form 1065) are due March 15, but extensions are common across the industry — file your personal-return extension if your K-1 hasn't arrived by early April.

What is a Schedule K-1 Form & How Does it Affect Your taxable income?

The Schedule K-1 (Form 1065) is the IRS document a partnership uses to allocate its income, losses, deductions, credits, and distributions to its individual partners. In a multifamily syndication, the partnership entity — typically a Delaware or state-formed LLC taxed as a partnership — doesn't pay federal income tax itself. Instead, the entity files Form 1065 reporting its results to the IRS, and each partner receives a Schedule K-1 showing their pro-rata share of those results. The LP then takes the K-1 numbers and reports them on their personal return (Form 1040, Schedule E).

The General Partner (GP), also called the sponsor or syndicator — Willowdale in our deals — is responsible for preparing the 1065 and issuing the K-1s. The LPs (limited partners or passive investors) receive their K-1s and pass them through to their own CPA for personal-return integration. The economic substance flowing through the K-1 is identical to direct property ownership: depreciation, interest deductions, and operating expenses pass through to the LP just as if they owned the property individually, scaled by their ownership percentage.

The math on a simple deal: $1,000,000 of partnership net income, two equal partners, each partner's K-1 shows $500,000 of income. In a real syndication the allocation is more nuanced — the partnership agreement (the operating agreement and the offering documents) defines waterfalls, preferred returns, profit-share tiers, and allocations that may differ from raw ownership percentage. But the K-1 mechanic is the same: it's how the partnership tells the IRS who owes tax on what.

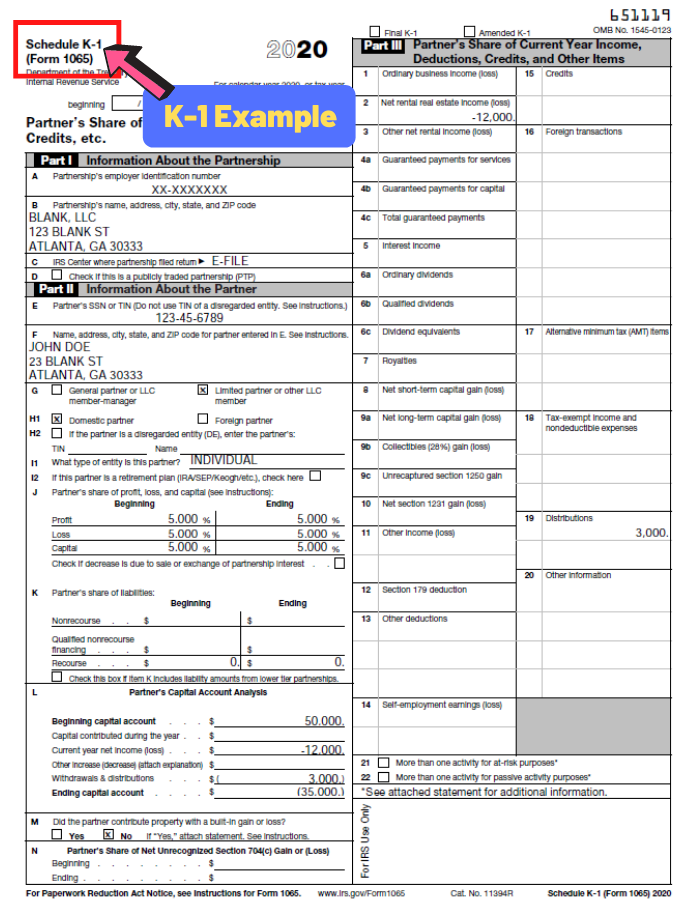

Schedule K-1 Form Sections You Should Know

Four boxes on the Schedule K-1 carry the information a passive multifamily LP actually needs to read. The other 30+ fields exist for partnerships with more complex tax situations — foreign partners, oil and gas income, charitable contributions, §179 deductions — but for a typical multifamily LP, the four below are the operative ones. (To pull a blank form for reference, the IRS publishes it at irs.gov/pub/irs-pdf/f1065sk1.pdf.)

- Box J — Partner's share of profit, loss, and capital (your ownership percentage)

- Box 2 — Net rental real estate income (loss) (the net tax figure after depreciation)

- Box 19 — Distributions (actual cash you received)

- Box L — Partner's capital account analysis (running ledger of basis, contributions, withdrawals)

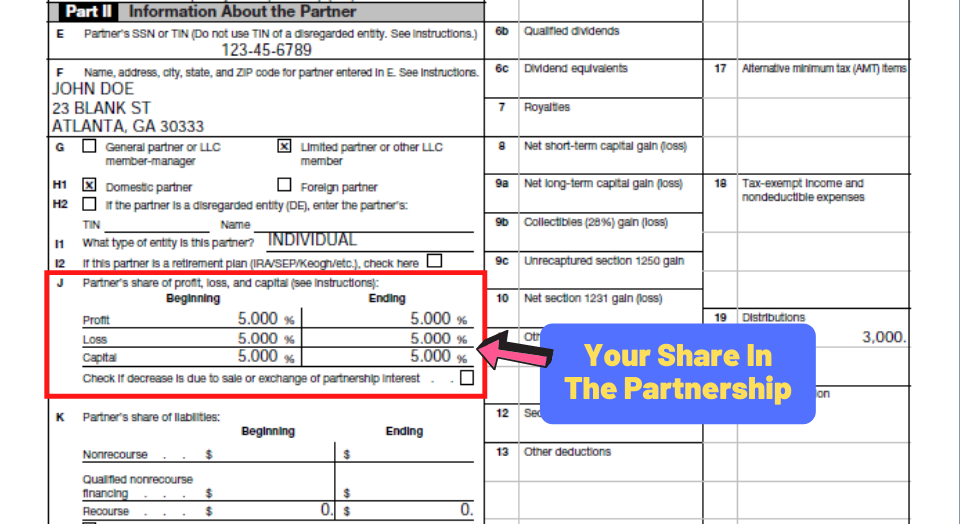

Box J - Partners share of profit, loss, and capital

Box J shows the LP's percentage ownership of the partnership — broken out into beginning-of-year and end-of-year shares of profit, loss, and capital. In a typical syndication, those three percentages are equal at the LP level: if an LP invested $50,000 into a $1M raise, they own 5% of profits, 5% of losses, and 5% of capital. The numbers can differ in more complex structures — preferred equity tiers, sponsor promotes, capital calls that diluted some LPs but not others — but for a vanilla Class A LP position in a multifamily deal, the three figures line up.

Box J is the multiplier on almost everything else that flows through the K-1. The partnership reports its full Box 2 income/loss, full Box 19 distributions, and Box L capital account at the partner level, but those numbers are already pro-rated by the LP's Box J percentage. Understanding Box J makes the rest of the form make sense.

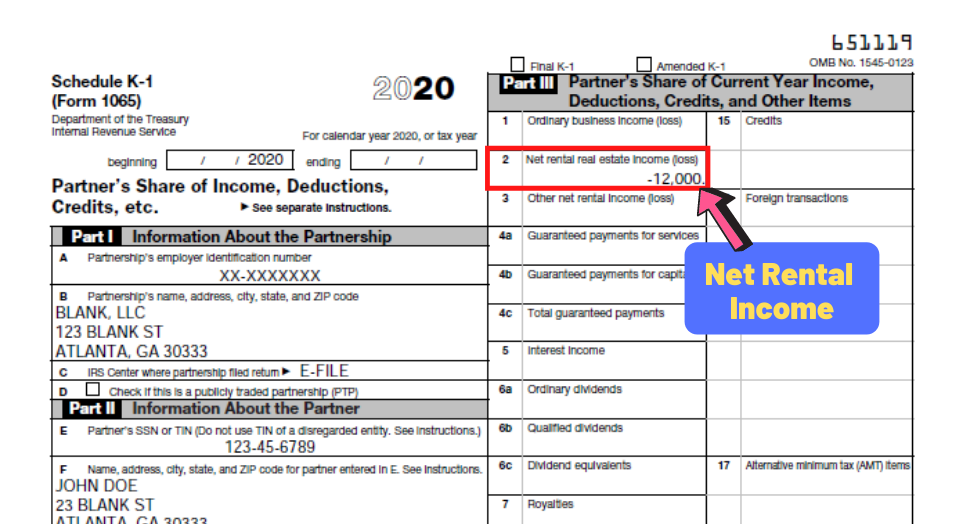

Box 2 - Net rental real estate income (loss)

Box 2 reports the LP's pro-rata share of the partnership's net rental real estate income — the calculated tax figure, not the cash. The math is: gross rental revenue, minus all operating expenses, minus interest expense on the property loan, minus depreciation, minus all other allowable deductions. Depreciation is the biggest line item: on a value-add multifamily deal with a cost-segregation study, accelerated depreciation in the first year alone can exceed the property's net operating income, producing a Box 2 number that's deeply negative even though the deal is generating positive cash flow.

That gap — Box 2 showing a paper loss while Box 19 shows real cash distributions hitting an LP's account — is the single most common point of confusion we see in K-1 review season. An LP receives $3,000 in actual distributions during the year (Box 19) and a K-1 showing a $12,000 loss (Box 2), and the natural reaction is “wait, am I losing money on this?” No — the loss is non-cash. The depreciation deduction shields some or all of the actual cash income from tax, and depending on the LP's tax situation, the loss can pass through to offset other passive income or carry forward to future years.

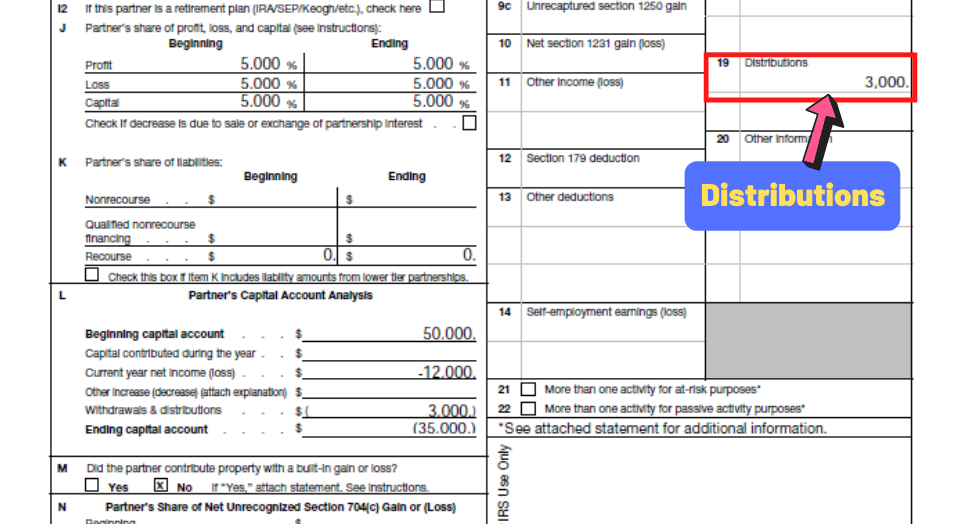

Box 19 - Distributions

Box 19 reports the cash distributions the partnership paid to the LP during the year — the literal money that moved from the syndication's operating account to the LP's bank account. In a stabilized multifamily deal distributing monthly or quarterly preferred returns, Box 19 is roughly the cumulative annual cash received. Refinance distributions, capital event distributions, and sale proceeds also flow through Box 19 in the year they're paid.

The critical point for an LP reading their K-1 for the first time: Box 19 is not the same as Box 2. Box 19 is cash. Box 2 is the tax calculation. A typical first-year-of-hold pattern for a value-add multifamily deal is Box 19 showing $2,000–$4,000 of distributions on a $50,000 investment (the 4–8% cash-on-cash typical of stabilized cash flow) while Box 2 shows a negative number because the depreciation deduction exceeds the deal's net taxable income. Box 19 cash is not double-counted into Box 2 — the partnership's reporting separates real economic cash flow from the tax-allowable income figure deliberately.

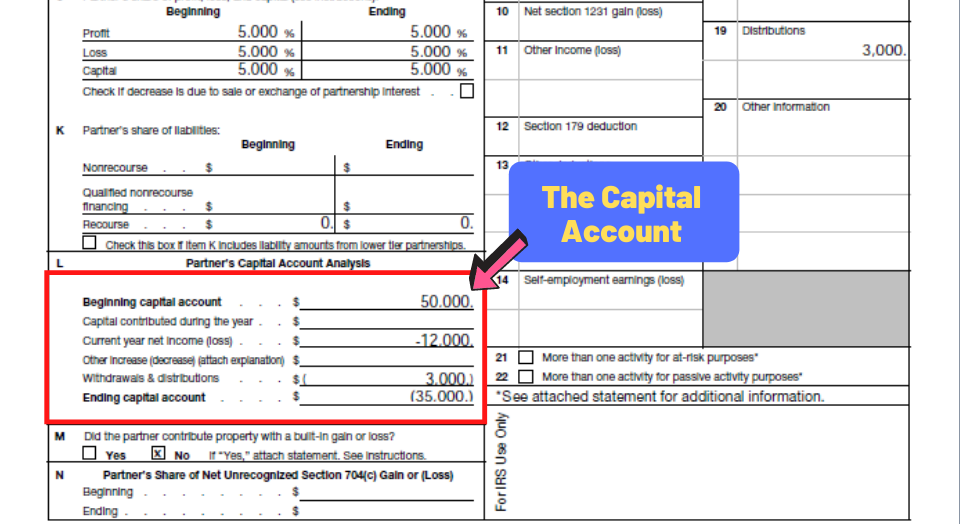

Box L - Partner's capital account analysis

Box L is the running ledger of the LP's capital account in the partnership. It tracks four moving parts year over year: beginning capital, capital contributions during the year, current-year net income or loss, and withdrawals and distributions. The ending capital account at year-end is the starting number for the following year's K-1.

Box L is where the cumulative arithmetic of the investment shows up. An LP who invested $50,000 starts with $50,000 in “Beginning capital account” (year 1: $0 beginning + $50K contribution). During the year, they receive $3,000 in distributions (drawn down) and absorb a $12,000 paper loss (drawn down). Their ending capital account is $50,000 + $0 − $3,000 − $12,000 = $35,000. That doesn't mean their investment is “worth” $35,000 — Box L is a tax-accounting figure, not a market valuation. It is, however, the figure that gets reconciled to compute the LP's tax basis (which the LP's CPA further adjusts for the partner's pro-rata share of partnership debt, per the rules on basis-for-nonrecourse-debt).

When should I receive my K-1?

The partnership's Form 1065 is due to the IRS by March 15 (the 15th day of the third month following year-end, for calendar-year partnerships). Schedule K-1s are issued to LPs as part of that filing. In practice, the K-1 timeline depends on how clean the partnership's books are, how complex the year was (acquisitions, refinances, dispositions, cost-segregation studies all complicate the return), and the CPA firm's capacity through tax season.

LPs in a typical multifamily syndication should plan for K-1 arrival between mid-March and early April. Some sponsors hit the March 15 deadline cleanly; others file partnership-level extensions (Form 7004) that push the K-1 timeline into April or, in unusual cases, beyond. Willowdale's target is to get K-1s to our LPs by mid-to-late March each year, but partnership tax filings are complex and timelines do flex with the realities of the year.

If an LP needs to file their personal return and their K-1 hasn't arrived, they can file Form 4868 for an automatic six-month personal-return extension. This is common practice across the syndication investor base — many LPs file extensions every year purely to align with K-1 timing, then complete their personal returns once all the partnership K-1s are in hand.

Is rental income passive income?

Yes — the IRS treats rental real estate activity as passive by default under §469 of the Internal Revenue Code, regardless of how much time the investor spends managing the property. Passive losses can only offset passive income or capital gain at sale; they cannot offset W-2 wages or other active-business income on the personal return. Suspended losses (passive losses that exceed current-year passive income) carry forward indefinitely and become deductible against future passive income or upon disposition of the underlying activity.

There is one significant carve-out: real estate professional status (REPS) under §469(c)(7). REPS-qualified taxpayers — those who spend more than 750 hours per year and more than half their working time materially participating in real estate trades or businesses — are exempt from the passive activity loss rules. Their real estate losses become active losses and can offset W-2 or other active income. We'll come back to REPS in the loss section below.

The Yield Brief · Free Weekly Newsletter

Multifamily markets, rates, and policy — for accredited investors. 2k+ subscribers.

K-1 net rental real estate income

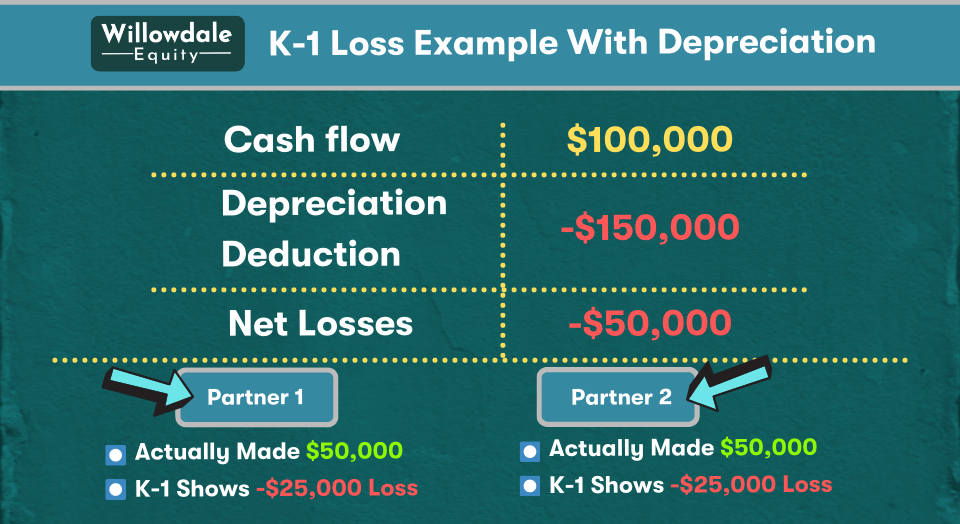

The Schedule K-1's most LP-relevant feature is the depreciation pass-through that produces the Box 2 paper loss. The IRS allows residential rental real estate to be depreciated over 27.5 years (39 years for commercial). On a $10M apartment building, that's roughly $290,000 of annual straight-line depreciation against the net operating income — a substantial deduction that frequently turns a cash-flow-positive deal into a tax-loss-positive deal on paper.

The depreciation gets bigger when the partnership commissions a cost-segregation study. Cost-seg is an engineering analysis that reclassifies portions of the building — interior finishes, fixtures, land improvements, certain electrical and plumbing components — from 27.5-year property into 5-, 7-, or 15-year property eligible for accelerated depreciation. The reclassified portion can be deducted on an accelerated schedule, and under current bonus depreciation rules, a significant portion can be deducted in year one. The result is a much larger Box 2 paper loss in the early years of the hold than straight-line depreciation alone would produce.

Numerical example: a property generates $100,000 in cash flow during the year. The partnership claims $150,000 of depreciation against that cash flow. The Box 2 net rental income figure is −$50,000 (a paper loss). With two equal partners, each partner's K-1 shows a $25,000 paper loss in Box 2 — even though each partner received $50,000 in actual cash flow during the year (reported in Box 19). That's the structural mechanic that makes leveraged multifamily syndication tax-efficient: the cash flow is real, the loss is real for tax purposes, and the LP gets both.

How is K-1 income taxed and the passive income tax rate

K-1 income from a multifamily syndication is taxed at the LP's marginal income tax rate as passive income, with one important wrinkle: the Box 2 figure is the net number after depreciation, not the gross cash flow. If Box 2 is positive, the LP pays their marginal federal rate on it (plus state tax if their state has an income tax — Texas LPs in TX-only deals owe no state tax; Georgia LPs in GA deals owe Georgia state income tax on the GA-allocated portion). If Box 2 is negative, the LP has a passive loss that offsets other passive income or carries forward.

The LP does NOT separately pay tax on the Box 19 distributions. Cash distributions in a partnership are not income for tax purposes — they're a return of partnership cash that's already been allocated for tax in Box 2. This is one of the structural distinctions between a syndication K-1 and, say, a REIT dividend (which is taxed when received, even though the REIT internally depreciates its assets). With the K-1 structure, the LP is taxed on the partnership's net taxable income, not on the cash they actually received. The two diverge through depreciation.

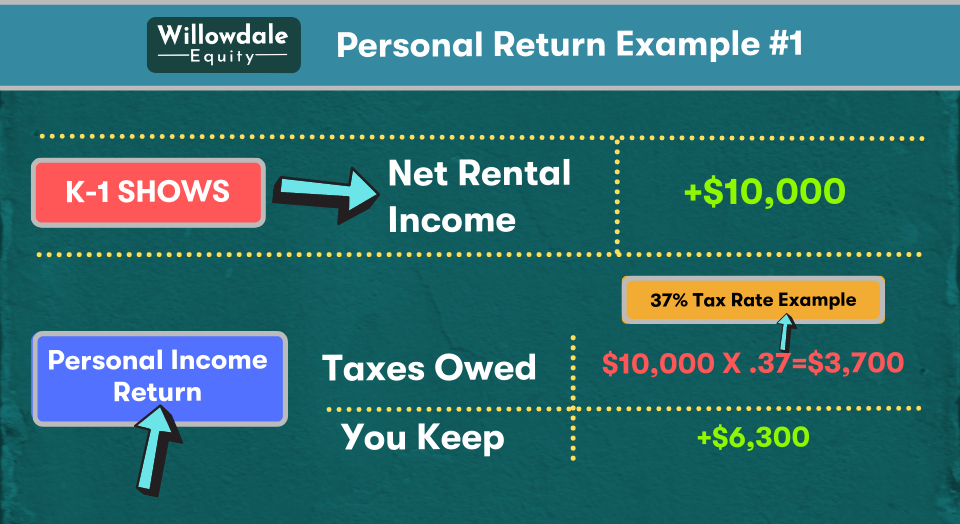

How is K-1 income taxed for real estate investors: [Example 1]

Scenario: LP receives a K-1 with Box 2 showing $10,000 of net rental real estate income for the year. LP is in the 37% federal marginal bracket. On their personal return, the $10,000 flows to Schedule E and is added to their other taxable income. Federal tax owed on this slice of income: 37% × $10,000 = $3,700. State tax depends on where the property is and where the LP resides. After tax, the LP keeps $6,300 of the $10,000.

That's the textbook case where Box 2 is positive — which happens in stabilized later-hold years when depreciation has slowed and net operating income exceeds the remaining annual deduction. It's also what happens on the disposition year, when sale proceeds and any depreciation recapture flow through. In the early years of a value-add hold, Box 2 is more frequently negative.

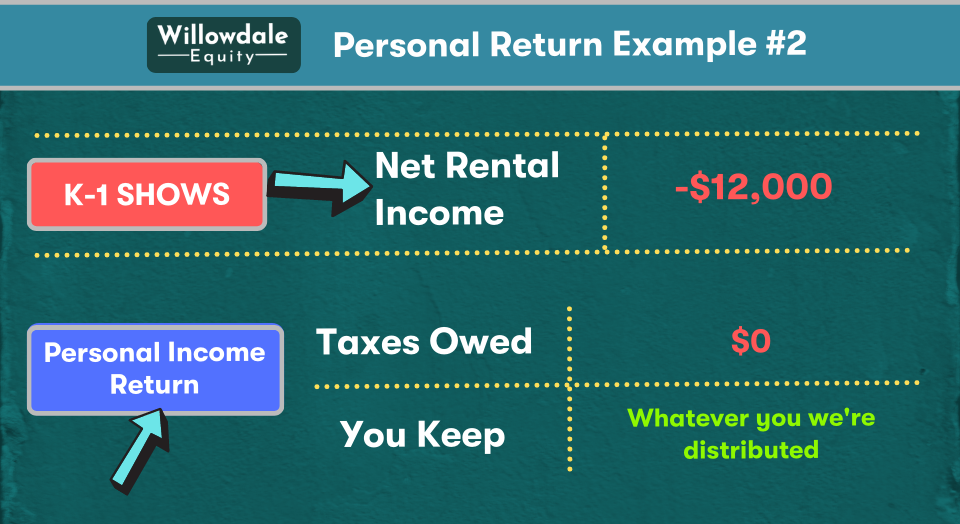

How is K-1 income taxed for real estate investors: [Example 2]

Scenario: LP receives a K-1 with Box 2 showing a −$12,000 paper loss for the year. Box 19 shows that the LP received $3,000 in cash distributions during the same year. The cash distribution is not separately taxed; the tax effect for the year is the $12,000 passive loss. If the LP has $12,000 or more of other passive income that year (from another syndication, another rental property, a real estate partnership), the loss offsets it dollar-for-dollar, dropping their passive-income tax bill to zero. If they have no passive income to offset, the loss is suspended and carried forward to future tax years.

The structural takeaway: the LP received $3,000 in real cash, owes $0 of tax on the partnership income for the year, and has a $12,000 carryforward loss available against future passive income. That's the tax-efficient passive vehicle that makes multifamily syndication attractive to high-income accredited investors.

Business income, ordinary income for the tax professional. What you need to do with a Schedule K-1

One scenario where K-1 income is taxed differently is when the LP holds the partnership interest inside a tax-advantaged account — a self-directed IRA, a Solo 401(k), or another retirement vehicle. The general rule is that retirement-account-held investments are tax-deferred (traditional) or tax-free (Roth), but there's a carve-out for what the IRS calls Unrelated Business Taxable Income (UBTI) and Unrelated Debt-Financed Income (UDFI).

UBTI applies when a tax-exempt entity (including an IRA) earns income from an “unrelated trade or business” — meaning a business activity unrelated to the entity's exempt purpose. Operating businesses run through a partnership generate UBTI when their income flows to an IRA-LP. UDFI applies when an IRA-held investment uses borrowed money to acquire income-producing property — the income attributable to the leveraged portion is subject to tax even inside the IRA.

For passive multifamily syndication LPs investing through an SDIRA, UDFI is the relevant issue: the property is financed with agency debt, the leveraged portion of the income flows through the K-1 to the IRA, and the IRA owes tax on that piece via Form 990-T. The mechanic doesn't necessarily kill the investment math — leveraged multifamily inside an SDIRA still benefits from the depreciation shield against the UDFI calculation — but it's a wrinkle worth raising with your CPA and your SDIRA custodian before subscribing.

How does K-1 loss affect my taxes?

K-1 losses from a multifamily syndication are passive losses by IRS classification. For an LP whose income comes primarily from a W-2 or active-business source, the passive losses on the K-1 can only offset other passive income — not the W-2 paycheck. The losses don't disappear if there's no current-year passive income to offset; they suspend and carry forward indefinitely until either (a) the LP has future passive income to absorb them or (b) the LP disposes of the underlying syndication interest, at which point the suspended losses unlock and become deductible.

The exception that high-income real estate investors structure around is real estate professional status (REPS). Under §469(c)(7), a taxpayer who spends more than 750 hours per year and more than half their personal-service working time materially participating in real estate trades or businesses qualifies as a real estate professional, and their rental real estate activity becomes non-passive. REPS-qualified taxpayers can use rental real estate losses to offset W-2 active income — a powerful tax shield for high earners who can structure their working time accordingly.

The well-known REPS pattern in the syndication LP community is the spouse pairing — a high-W-2-earner spouse (often a physician, attorney, or executive) and a stay-at-home or part-time-working spouse who qualifies as the real estate professional by spending the requisite hours managing direct rental properties or syndication assets. A widely-circulated example involves a doctor earning $3M of active W-2 income whose spouse, qualifying as the real estate professional, generated enough depreciation losses from a real estate portfolio to offset the entire $3M of active income. The IRS challenged the position and lost. We've heard of LPs pursuing this structure in private real estate generally — though structuring it requires meeting the hour-and-participation tests strictly, and it's a structure that goes through your CPA, not your syndication sponsor.

Free 5-Day Video Course

Everything you need to evaluate passive multifamily — in five short videos.

Five 7 a.m. emails over five mornings. Earned-vs-passive income, syndication mechanics, K-1 tax treatment, market cycles, and underwriting — no credit card, no sales pitch.

Get Instant Access →Free. Unsubscribe with one click.

The Tax Implications of Different Structures:

The entity type that holds the investment determines the tax treatment, even when the underlying economic activity is identical. The five most common entity structures an accredited investor will encounter — partnerships, S corporations, C corporations, trusts and estates, and LLCs — each have distinct tax characteristics that affect how K-1 (or equivalent) income flows to the individual.

Partnerships

Partnerships are pass-through entities for federal tax purposes. The partnership itself files Form 1065 and issues Schedule K-1s but pays no federal income tax. Each partner's pro-rata share of partnership income, deductions, credits, and distributions flows through to their personal return. This is the structure underlying virtually every multifamily syndication, including Willowdale's — the operating LLC is taxed as a partnership precisely so the deal's depreciation and operating losses can pass through to the LPs efficiently.

S Corporations

S corporations are also pass-through entities but with more restrictive rules. Profits and losses pass through to shareholders on Schedule K-1 (Form 1120-S), but S-corp shareholders can also be employees, in which case they receive both W-2 wages (subject to FICA payroll tax) and a K-1 distribution share (not subject to FICA). The S-corp structure is rarely used for real estate syndication because it doesn't accommodate the partnership flexibility needed for waterfalls, preferred returns, and tiered profit-share — partnerships under Subchapter K are the dominant structure for that reason.

C Corporations

C corporations are separate taxable entities. The C-corp files Form 1120 and pays federal income tax at the corporate rate (21% currently). When the C-corp distributes after-tax profits to shareholders as dividends, the shareholders pay tax again at their individual qualified-dividend or ordinary-income rate — the “double taxation” feature that makes C-corps a poor match for real estate-holding entities. C-corps are common in operating businesses with retained-earnings strategies (tech companies, manufacturers, capital-intensive operators that want to defer distributions) but rare in syndicated multifamily, where the goal is efficient pass-through of depreciation to high-tax-bracket LPs.

Trusts and Estates

Trusts and estates file Form 1041 and may receive K-1s from partnerships in which they hold interests. Income retained inside the trust is taxed at the trust's compressed federal brackets — which reach the top 37% rate at roughly $15,000 of taxable income, much faster than individual rates. Income distributed to beneficiaries flows out to them via Schedule K-1 (Form 1041) and is taxed at the beneficiary's individual rate. Many high-net-worth investors hold syndication interests inside revocable living trusts, irrevocable trusts, or family LLCs for estate-planning reasons; the partnership K-1 then flows to the trust's 1041, and the trust's beneficiaries see the partnership income on the trust K-1.

Limited Liability Company (LLC)

An LLC is a legal entity, not a tax classification. By default, a single-member LLC is disregarded for federal tax purposes (its income flows directly to the member's personal return), and a multi-member LLC is taxed as a partnership (Form 1065 + Schedule K-1s). An LLC can also elect to be taxed as an S corporation or C corporation by filing Form 2553 or 8832, respectively. For multifamily syndications, the operating entity is almost always a multi-member LLC taxed as a partnership — combining the legal liability shield of an LLC with the pass-through tax efficiency of a partnership.

The Consequences of Filing Extensions

Partnership returns (Form 1065) are due March 15 for calendar-year filers. When a partnership needs more time, it files Form 7004 for an automatic six-month extension, pushing the return deadline to September 15. The K-1s flow with the return, so an extended partnership timeline can mean LPs don't receive their K-1s until later in the spring or summer. The practical consequence for LPs is on the personal-return side — extending the partnership return doesn't automatically extend the LP's personal return, and the personal return remains due April 15 (or October 15 with extension).

1.) Late Filing Penalties:

If an LP files their personal return after April 15 without filing an extension (Form 4868), the IRS assesses a failure-to-file penalty of 5% of unpaid tax per month, up to 25%, plus interest. The simplest mitigation when a K-1 is delayed: file the LP's personal extension by April 15. The personal extension gives until October 15 to file the return — typically more than enough time for even a delayed K-1 to arrive. Note that the extension extends the filing deadline only, not the payment deadline: any tax owed is still due April 15, so LPs may need to estimate their syndication K-1 numbers (the sponsor can usually provide a preview figure) and pay any estimated tax with the extension to avoid underpayment penalties.

2.) Interest Accrual:

Interest on unpaid tax accrues from the original April 15 due date until the tax is paid in full, regardless of whether an extension is on file. The IRS interest rate is set quarterly at the federal short-term rate plus 3%. To minimize interest, an LP whose K-1 is delayed should estimate the partnership's results conservatively, pay any estimated balance with the personal extension by April 15, and reconcile when the K-1 arrives. Overpayment is refunded; underpayment continues to accrue interest until paid.

3.) Incomplete or Inaccurate Information:

Reviewing the K-1 for accuracy before integrating it into the personal return is essential. The LP's name, EIN/SSN, ownership percentages, capital account beginning and ending balances, and the Box K liability share are all worth verifying against subscription documents and prior-year K-1s. Errors are most common in the year after a refinance, sale, or major capital event. If anything looks wrong, the LP's CPA should contact the sponsor's CPA directly to request an amended K-1 before filing — amended K-1s are common and unremarkable when caught early; they become expensive (LP amended personal return required) when caught after filing.

Frequently Asked Questions About How Does a K1 Affect My Personal Taxes

Do you pay taxes on k1 income?›

You pay tax on the Box 2 net rental real estate income figure on your K-1 if that number is positive — at your marginal federal income tax rate, plus any state income tax owed where the property is located. If Box 2 is negative (a passive loss), you owe no current-year tax on the partnership income; the loss either offsets other passive income or carries forward to future years. Cash distributions reported in Box 19 are not separately taxed — they're a return of partnership cash that's already been allocated for tax in Box 2.

Are K 1 distributions considered income?›

Not in the way most LPs initially expect. The Box 19 cash distributions you received during the year are not separately taxed — they're treated as a return of partnership cash that's already been allocated to you for tax purposes via the Box 2 net income figure. The taxable event is the Box 2 number, not the Box 19 cash. The two can diverge significantly: in early years of a value-add hold, Box 19 cash is often positive while Box 2 shows a paper loss from accelerated depreciation.

Can k1 losses offset w2 income?›

Not by default. K-1 losses from rental real estate are passive losses under IRS §469, and passive losses can only offset other passive income — not W-2 wages or other active income. The carve-out is real estate professional status (REPS) under §469(c)(7): if you (or, more commonly, a spouse) spend 750+ hours per year and more than half your personal-service working time materially participating in real estate trades or businesses, the rental losses become active and can offset W-2 income. REPS qualification is strict — it goes through your CPA, with documented hour tracking, not your syndication sponsor.

How Is K1 Income Taxed - Conclusion

The Schedule K-1 is the primary tax document an LP receives from a multifamily syndication, and reading it accurately is part of the literacy that distinguishes a comfortable passive investor from one constantly emailing their sponsor for explanations. The four-box framework — Box J ownership, Box 2 net income, Box 19 distributions, Box L capital account — covers everything a typical LP needs to integrate into their personal return. The bigger conceptual move is to internalize that the Box 2 paper loss and the Box 19 cash distributions are reporting different things, and that the gap between them is the depreciation shield that makes leveraged multifamily syndication tax-efficient.

For LPs who are new to syndication tax mechanics, the practical first steps are: (1) build a working relationship with a CPA who has read syndication K-1s before, (2) plan on filing a personal-return extension every year purely to align with K-1 arrival timing, (3) expect the Box 2 paper loss to often exceed Box 19 cash in the early years of a value-add hold, (4) keep prior-year K-1s for basis tracking, and (5) ask the sponsor for a preview K-1 figure by mid-March so the personal-return extension can include an accurate estimated payment. The K-1 is the document that turns a syndication investment from “rental income” into a structurally tax-advantaged passive vehicle — the literacy is worth investing in.

First-Look Access

Get on the list for the next acquisition.

Our investor club members get first look at every new Class B & C value-add multifamily deal we underwrite — before the soft-reservation list opens publicly.

Daniel Di Cerbo

Daniel is the Co-Founder and Principal of Willowdale Equity, a private real estate investment firm specializing in Class B & C value-add multifamily assets across the Southeastern U.S. He has been a sponsor on over $150M of multifamily acquisitions across Georgia and Texas.

Willowdale Equity content follows strict guidelines for editorial accuracy and integrity. Learn more about our editorial guidelines.