Table of Contents

- Passive Real Estate Investing Guide to Multifamily Syndication

- Why multifamily real estate?

- What is a multifamily syndication?

- Why invest in a multifamily syndication?

- How is a multifamily syndication structured?

- Who can invest in an apartment syndication?

- How can I invest in a passive real estate investment like a multifamily syndication?

- Syndication vs. REIT

- Syndication vs the stock market

- Why real estate is the best passive income?

- How do you get into passive real estate?

- The 3 ways we build equity and add value to an apartment community

- The 4 types of multifamily real estate investing strategies

- Frequently Asked Questions About Passive Real Estate Investing

- Getting Started With Passive Real Estate Multifamily

Passive investing in multifamily real estate is the structure that lets an accredited investor capture the operating economics of institutional-grade apartment assets — the cash flow, the depreciation that shelters that cash flow, the equity built through both forced and market appreciation — without taking on the operational reality of being a landlord or a multifamily operator. The vehicle is the multifamily syndication: a private partnership where an experienced sponsor sources the deal, signs the debt, executes the value-add business plan, and reports to a group of limited partners (LPs) who provided the bulk of the equity in exchange for a pro-rata share of the economic outcomes.

For a busy professional whose primary income comes from a W-2 or an operating business, the syndication structure solves a real problem. Building a meaningful direct real estate portfolio — finding the deals, underwriting them, lining up the debt, executing the business plan, and managing tenants — is a full-time job that competes for the same time and attention that produces the original income stream. Becoming an LP in a syndication preserves the income stream by letting professional operators run the property, while the LP captures most of the same after-tax economics that a direct owner would.

This guide walks through the full LP-onboarding picture: how syndications work, why multifamily as an asset class, the seven economic reasons sophisticated LPs gravitate to the structure, how it compares to public REITs and direct stock market exposure, who can legally participate under SEC rules, the practical mechanics of how the equity is structured, the three ways operators actually build equity in an apartment community, the four investment-strategy categories you will encounter when evaluating deals, and how to take the first step.

Key Takeaways

- Passive investing in multifamily real estate via syndication gives an LP the cash flow, depreciation, and equity-growth benefits of direct ownership without the operating responsibility. The structure pools accredited investor capital alongside an experienced sponsor who runs the property under a value-add business plan, with LPs typically receiving 70–75% of the equity in exchange for putting up most of the capital.

- The seven economic reasons LPs gravitate to the structure compound: pass-through depreciation shelters taxable distributions, the asset class hedges inflation through rising rents and a fixed-rate mortgage, agency leverage amplifies returns, distributions arrive monthly or quarterly, true passive income preserves the LP's primary career, the risk-adjusted return is strong relative to public markets, and equity grows through both forced appreciation and amortization across a 5–7 year hold.

- The structural alternative to syndication for most accredited LPs is a public REIT or direct stock market exposure. Both are more liquid, but neither passes through the depreciation that shelters cash distributions on a syndication K-1, and neither produces the post-tax yield differential we walk through in the worked example below.

Passive Real Estate Investing Guide to Multifamily Syndication

The guide that follows is structured for an accredited investor evaluating multifamily syndication for the first time, or for a sophisticated investor sanity-checking the structure against direct ownership, public REITs, or other passive income alternatives. We move from the basic mechanics (what a syndication is, how it is structured, what each party does) through the economic case (why multifamily specifically, the tax and inflation properties of the structure, the comparison to other passive income vehicles) to the practical execution (who is legally eligible to participate, what the investment strategies mean, how to take the first step).

The audience matters because the LP perspective is different from the operator perspective on every section that follows. We are writing as multifamily operators — the syndicators on the other side of the LP relationship — but the framing throughout is what an LP needs to understand to evaluate a deal and an operator, not what an operator needs to know to execute one. If you are evaluating passive investments and the analysis below seems heavier than typical introductory content, that is intentional. Most LPs who get into trouble do so because they evaluated a sponsor and a deal on superficial signals (projected IRR, marketing polish) without understanding the underlying mechanics.

Why multifamily real estate?

Multifamily real estate sits at the most resilient end of the commercial real estate spectrum because housing is non-discretionary demand. People will downsize, double up, move to lower-cost markets, or shift between owning and renting, but the underlying need for shelter does not go away through economic cycles. That demand resilience shows up empirically: across the past several decades, multifamily has produced less volatility than every other major commercial real estate asset class while delivering the best risk-adjusted returns. The COVID-19 demand stress test in 2020 made the contrast unusually clear — student housing collapsed as universities went remote, office buildings emptied, retail accelerated its e-commerce-driven decline, and senior living faced operational and demand challenges, while multifamily collections held in the 90%-plus range across most institutional portfolios.

The structural support for multifamily demand is unusually durable across three dimensions: a rising base of higher-income renters, a meaningful structural undersupply relative to demand, and demographic tailwinds from both Millennials/Gen Z and net new migration into the U.S. The charts below illustrate the magnitude of each.

% of Apartment Households Earning Greater Than $75,000/Year

According to the National Multifamily Housing Council, the higher-income segment of the renter population (households earning $75,000 a year or more) has grown from roughly 18% of total renters across 1990–2010 to over 25% in 2020. The shift toward higher-earning renters is what supports continued long-term rent growth in well-located multifamily markets — a tenant base with higher incomes can absorb meaningful rent increases without compromising occupancy.

Annual New Supply Required to Keep up with Forecasted Demand Growth

The National Apartment Association and the National Multifamily Housing Council have estimated that the U.S. needs roughly 328,000 new apartment units delivered annually to keep pace with renter demand. Actual delivery over the past decade has averaged around 239,000 units a year — a structural gap that compounds annually. The gap is constrained by rising construction costs, which only pencil for Class A luxury product at current cost levels, meaning the structural undersupply is concentrated in workforce and Class B/C inventory where the natural rent-paying demand actually sits.

Millennials & Baby Boomers Want To Rent

Households aged 18–34 (Millennials and the older edge of Gen Z) are now the largest single segment of the renting population — roughly 39 million renters across that band. Total U.S. renters have crossed 100 million for the first time, an all-time high that the National Apartment Association expects to continue growing. Net new migration is projected to account for roughly half of that growth: 70% of immigrants who arrived in the U.S. over the past decade chose to rent rather than buy, which sustains baseline multifamily demand even before the domestic demographic growth is layered on.

What is a multifamily syndication?

A multifamily syndication is a private partnership that pools capital from a group of passive limited-partner investors (LPs) alongside an experienced general partner (GP, also called the sponsor or syndicator) to acquire an apartment property that none of them would buy individually. The capital stack typically comes together as 70–75% senior debt (most often agency debt from Fannie Mae or Freddie Mac via the DUS and Optigo programs, sometimes a bank or bridge loan on value-add or rehab-heavy deals) and 25–30% equity. The equity portion is what the GP raises from the LP base, with the GP itself typically contributing a small portion of the equity check alongside the LPs to demonstrate alignment.

The structure is almost always a single-purpose LLC that holds the property, with the GP entity as the manager and the LPs as members. Many parties surround a typical syndication transaction — CPAs, lenders, real estate brokers, attorneys, property managers, and the sponsor entity that puts the deal together and signs the loan — but from the LP's perspective the structure is straightforward: write a check, become a member of the LLC, receive distributions and a K-1, and wait for the eventual refinance or sale event.

Passive real estate investing through this structure is meaningfully different from direct ownership. The LP receives the economic benefits of ownership — the cash flow, the pass-through depreciation, the share of appreciation — without taking on any of the operational responsibility for the property. The GP signs the debt, hires the property management company, executes the business plan, and absorbs all of the day-to-day decision-making. The LP's only ongoing involvement is reading the monthly or quarterly distribution reports.

Managing Rental Properties

The operational difference between single-family rental ownership and multifamily ownership at scale is one of the most underappreciated drivers of investor outcomes. A single-family rental requires a property manager to handle one tenant at one site, and the per-property management fee runs 8–12% of gross rent — a meaningful drag on cash flow that grows with portfolio size. Multifamily property management runs at a meaningfully lower per-unit fee because the management company can amortize the on-site staffing (leasing office, maintenance team, regional supervisor) across a hundred or more units in one location.

The practical consequence is that a multifamily LP gets professional, full-time on-site property management as part of the operating economics of the deal, while a direct single-family rental owner is either doing the work themselves or paying a meaningful management fee on every property. The quality of the property management company is the most important operational variable for an LP to understand before subscribing — the business plan disclosed in the PPM only executes if the on-site management team can actually run the property, and the difference between a high-quality regional PM and a generic national one shows up directly in collections, retention, and the rent-growth trajectory.

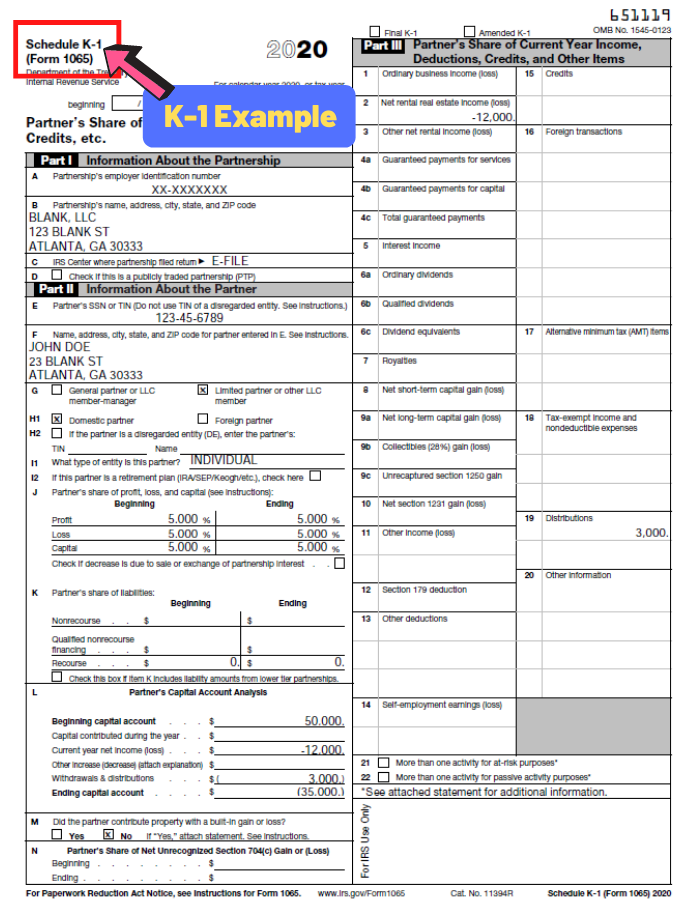

Schedule K-1

A Schedule K-1 is the partnership tax form that reports each LP's share of the syndication's income, losses, deductions, credits, and distributions for the year. The K-1 is issued by the partnership (typically delivered to LPs by mid-March each year), and the LP carries the relevant numbers from their K-1 onto their personal tax return. For a multifamily syndication LP, the K-1 is the operationally important document — it is what determines what tax actually gets paid on the cash distributions received during the year, and it is where the depreciation pass-through actually shows up.

The example K-1 above shows the four boxes that matter most for a multifamily syndication LP. Box J shows the LP's share of partnership profit, loss, and capital. Box 2 shows the net rental real estate income or loss flowing through to the LP — this is the number that determines taxable income, after depreciation has been applied. Box 19 shows distributions actually received during the year — the cash that hit the LP's bank account, which is meaningfully different from Box 2. Box L shows the partner's capital account analysis, which the LP's CPA reconciles to compute the tax basis applied to losses and distributions on the personal return.

One of the most common K-1 questions we receive from first-time LPs is why Box K (the LP's share of partnership liabilities, which reflects the pro-rata share of the property's nonrecourse mortgage) does not match the cash they actually wired in. The two are not supposed to match. Box K reflects the LP's allocated share of partnership debt, Box L is the book capital account, and the LP's tax basis is a third number entirely. None of the three equal each other after year one, and they are not supposed to — the LP's CPA reconciles all three to compute the tax-relevant basis applied to losses and distributions. We cover this in more depth in our guide to how the K-1 works in private real estate investing.

The pass-through-depreciation mechanic is what creates the post-tax yield differential between syndication and most other passive income vehicles. The K-1 Box 2 number is computed after the property's depreciation has been applied as a non-cash expense, which means an LP can receive meaningful cash distributions during the year while showing a net taxable loss on the K-1. Earned income from a W-2 or operating business is taxed at the LP's full marginal rate — multifamily syndication distributions, after depreciation pass-through, are often taxed at zero or close to it in the early years of a hold.

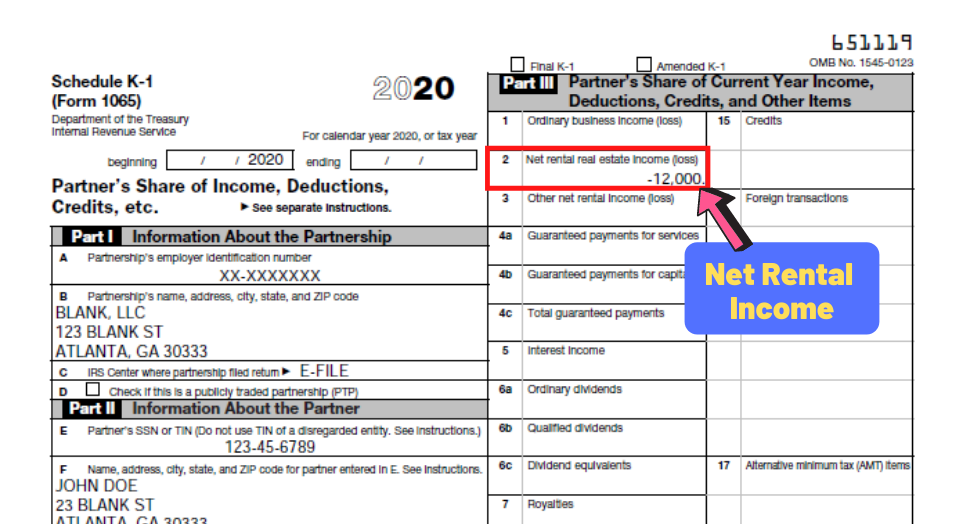

The image above shows what this looks like in practice: the LP received $3,000 in cash distributions during the tax year (Box 19), but the K-1 shows a $12,000 net rental loss in Box 2 because depreciation exceeded the property's net cash flow on a per-LP-share basis. The LP pays no tax on the $3,000 received, and the $12,000 loss can be carried forward to offset future passive income from the same or other real estate investments. This compounding pass-through shelter is the structural reason multifamily syndication is one of the most tax-advantaged passive income vehicles available to accredited investors.

Capital structure

The capital structure of a multifamily syndication deal is the organization and hierarchy of every dollar required to finance the acquisition. It splits into two buckets: debt (typically 70–75% of total capital) and equity (the remaining 25–30%). The equity itself often splits further into common equity (the standard LP investment) and preferred equity (a senior-equity slice that sits above common equity in the cap stack and earns a fixed return without participating in upside, typically deployed when the deal needs more capital than common LP equity alone can raise).

A worked example illustrates how the stack assembles. Suppose the deal is a $10 million, 150-unit garden-style multifamily community in a Sun Belt MSA. The senior debt covers 75% loan-to-value, or $7.5 million — typically agency debt with a fixed rate, 5- to 10-year term, and an interest-only period at the front end. The remaining $2.5 million covers the purchase price, plus roughly another $500,000 covers closing costs, lender-required prepaid reserves, operating reserves, acquisition fee, and other transaction expenses. The total equity raise lands around $3 million, or 30% of the purchase price.

That $3 million equity raise can be structured several ways depending on the deal. The most common is straight LP common equity — all $3 million in the same class, with the same preferred return and the same waterfall promote. Some deals introduce a preferred equity tranche (for example, $1.5 million common at 70/30 LP/GP split with an 8% pref and an IRR-based waterfall, plus $1.5 million preferred equity at a fixed 10% return with no upside participation). Preferred equity sits above common equity in the cap stack: it is paid out of cash flow and refinance/sale proceeds before any common equity distribution, which makes it a structurally safer position but caps the upside. Some LPs intentionally diversify across both classes within the same deal to spread their per-deal risk profile.

Why invest in a multifamily syndication?

Sophisticated LPs gravitate to multifamily syndication for a specific combination of structural reasons that compound. No single one of these reasons is the headline — what makes the asset class work as a passive income allocation is the combination of all seven operating together inside a single ownership structure. The sections that follow walk through each in turn.

1.) Tax benefits

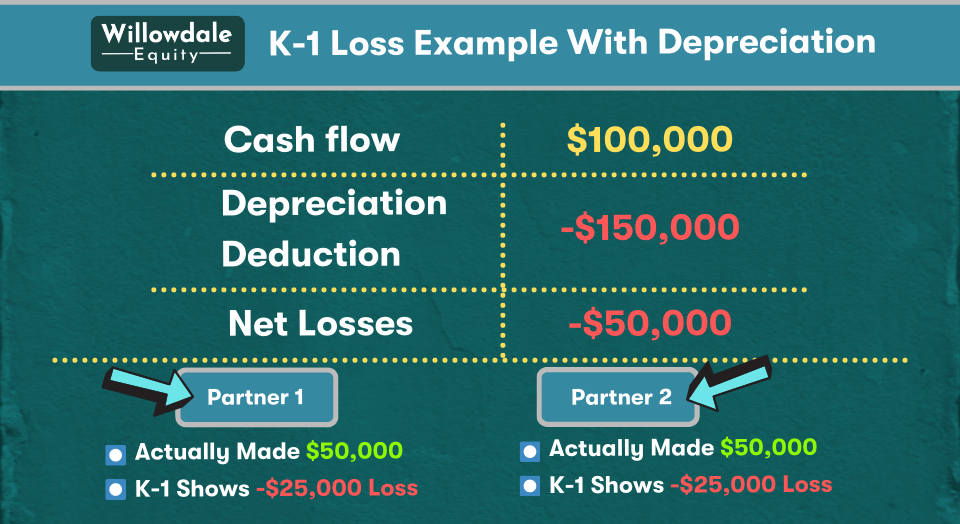

The single most important economic feature of multifamily syndication relative to most other passive income vehicles is the pass-through depreciation that flows through on the K-1. As an LLC member with direct economic ownership in the property, the LP receives a pro-rata share of the property's depreciation as a non-cash expense, which offsets the cash distributions received during the year. The structural effect is that an LP can receive meaningful monthly or quarterly cash distributions while showing a net taxable loss on their K-1.

The example above shows an LP who received $50,000 in cash distributions during the tax year, with a K-1 that reports a net rental loss because depreciation exceeded the property's net cash flow on the LP's share. Depreciation is the IRS-recognized decline of the building's value over the asset's useful life (27.5 years for residential rental property under straight-line depreciation, with cost segregation studies often accelerating a meaningful portion into earlier years via bonus depreciation on personal property and land improvements). The asset itself typically continues to appreciate in market value while the depreciation expense reduces taxable income on paper. The result for many multifamily syndication LPs is that the effective tax rate on their distribution income lands at zero or close to it for the first several years of a hold.

2.) Hedge against inflation

Multifamily real estate is one of the more reliable inflation hedges in private markets because both the revenue side and the debt side of the operating model move favorably when inflation runs above target. On the revenue side, residential leases typically reset every 12 months, which means rents reprice to current market levels on each renewal — in healthy submarkets, that reset usually exceeds the underlying inflation rate, which produces real revenue growth even after adjusting for the dollar's erosion. On the debt side, fixed-rate agency debt locks the loan payment at the closing rate for the full term, which means the LP's loan obligation is paid back in dollars that have meaningfully less purchasing power than the dollars that were originally borrowed.

The combined effect — rising nominal revenues against a fixed nominal debt payment — produces an NOI expansion that meaningfully exceeds inflation in any normal-to-elevated inflation environment. The cycle dynamic also matters: solid multifamily markets in the current cycle typically produce 2–3% organic rent growth annually before any value-add work, which keeps pace with or exceeds normal inflation. We discuss the cycle implications of inflation in more depth in our guide to buying real estate during recessions and to what assets do well in stagflation.

3.) Real leverage

Multifamily syndications use leverage in a way that direct stock investments cannot. The typical multifamily capital stack is 70–75% senior debt (almost always agency from Fannie Mae or Freddie Mac on stabilized institutional product, with fixed rates locked for 5 to 10 years and an interest-only period at the front end) and 25–30% LP equity. That leverage ratio is structurally available in real estate because the underlying asset is durable, the cash flows are predictable, and lenders are willing to extend long-duration credit against the cash flow stream.

The effect of leverage on LP returns compounds across the hold. A 6% unlevered yield on the property, levered 75% with debt at 6%, produces a meaningfully higher cash-on-cash yield on the LP's equity check — before any value-add work expands NOI. The same leverage that amplifies returns on the upside obviously amplifies downside in a stress scenario, which is why agency-debt discipline (fixed-rate, long-duration, non-recourse to the LP) matters: it protects the LP from rate-shock outcomes that bridge debt and floating-rate bank debt can introduce. In an inflationary environment, debt also works in the LP's structural favor — the loan is repaid in dollars that have lost purchasing power, which effectively transfers value from the lender to the equity holders.

4.) Steady cash flow

Multifamily syndications are structured to produce predictable monthly or quarterly cash distributions to LPs throughout the hold period. The cash flow comes from net operating income (NOI) after debt service, asset management fees, and required operating reserves, distributed pro-rata to LPs in accordance with the waterfall in the operating agreement. The typical structure pays LPs a preferred return (commonly 7–9%, cumulative-and-compounding) before the GP earns any promoted share above its asset management fee, which means LPs receive yield ahead of GP economics in any year where the deal generates distributable cash.

The cumulative-and-compounding mechanic on the pref is one of the most LP-friendly elements of a typical waterfall and worth understanding before subscribing. Cumulative means any year where cash flow falls short of the pref threshold accrues as a shortfall that gets paid in future years (or out of exit proceeds) before the GP receives any promote. Compounding means the unpaid pref earns its own pref the following year, which protects LPs in lower-cash-flow years (early-stage value-add, lease-up disruption, refinance years) by ensuring those shortfalls accumulate rather than reset annually. Simple non-compounding pref structures, by contrast, treat each year independently and can leave LPs structurally short of the headline pref rate by hold-end.

5.) True passive income

The “passive” in passive investing matters because most income labeled as passive by the financial industry is anything but. Direct rental property ownership requires the owner to handle property management, capital expenditure planning, tenant relations, eviction proceedings, and operational decisions throughout the year — the income arrives but the time commitment to produce it is meaningful, particularly as portfolio size scales. True passive income requires the investor to receive recurring cash flow without active involvement in the underlying asset's operations.

Multifamily syndication as an LP meets the strict definition: the GP signs the loan, manages the on-site staff and property manager, executes the value-add capex, handles the operational decisions, and reports to the LP base. The LP's involvement is reading the quarterly update, monitoring the distribution schedule, and at year 5–7 reading the disposition or refinance update. The time commitment is measured in hours per year, not hours per week, which is what makes the structure work for high-income professionals whose primary career is what produces the capital available to invest in the first place.

6.) Strong risk-adjusted return

Risk-adjusted return is the question of how much return per unit of risk an asset class produces, and multifamily syndication compares favorably to most public-market alternatives on this dimension over multi-cycle horizons. The reasons are structural: the asset class itself is unusually stable through cycles because housing demand does not collapse the way office or retail demand can, the agency debt market provides long-duration fixed-rate financing that protects equity from rate shocks, and the cash-flow stream from residential rents is predictable enough to plan around.

For a stabilized multifamily acquisition with 90%-plus occupancy, the risk profile is genuinely modest relative to most public equity exposure — the property is producing predictable cash flow on closing, the value-add work expands NOI further through the hold, and the eventual exit is supported by a deep institutional buyer base that creates real exit liquidity. Sponsors that underwrite to actuals (not broker pro formas) and target Maximum Allowable Offer discipline (the price that lets the deal weather a downturn and still pay healthy returns) produce risk-adjusted outcomes that public equity historically struggles to match across full cycles.

7.) Equity growth

Equity in a multifamily deal grows through three mechanics that compound across the hold: forced appreciation (NOI expansion from the value-add business plan, which directly increases the property's valuation at the prevailing cap rate), market appreciation (cap rate compression or rent growth driven by market conditions outside the operator's control), and amortization (monthly principal paydown on the senior debt, which converts debt into LP equity on the balance sheet). Each mechanic operates independently, and a competent operating year produces equity expansion from all three at once.

The growth is realized through one of two liquidity events in a typical 5- to 7-year hold: a refinance event (often around year 2 to 3 if the value-add work has progressed enough to support a larger loan, which can return a meaningful portion of LP capital while the property continues to be held for cash flow and further appreciation) and the eventual sale (year 5 to 7, where the accumulated equity from all three mechanics is monetized in full). At Willowdale's first multifamily acquisition — the 69-unit Mill Gardens property in Warner Robins, Georgia — the refinance at month 15 returned 62.5% of investor capital while the property remained held for continued cash flow and appreciation, illustrating how the equity-growth mechanics actually convert into LP outcomes in practice. We cover the three equity-creation mechanics in more depth in the section below.

How is a multifamily syndication structured?

Two parties form the partnership in every multifamily syndication: the General Partner (GP, also called the sponsor or syndicator) and the Limited Partners (LPs, the passive investors). The GP and the LPs together provide 25–30% of the total capital stack as equity, with the remaining 70–75% coming from senior debt. The equity itself is then split between GP and LP under the terms of the operating agreement, typically 70/30 or 60/40 LP/GP above the preferred return, with waterfall promotes that step up at IRR thresholds (for example, 70/30 to a 15% LP IRR, then 50/50 above).

The structural separation between GP and LP roles is intentional and is what makes the LP's investment passive. The GP handles every operational and financial decision; the LP provides capital and receives reports. The two parties are aligned on outcomes through the waterfall structure — the GP earns its promote only after the LP receives its preferred return and capital back, so the GP's incentive is to execute the business plan and produce strong outcomes for the LP base. The sections below walk through what each party actually does.

General Partner

The GP is the operating entity that puts the syndication together and manages the property through the hold. Their responsibilities are end-to-end: sourcing the deal (typically by reviewing 100-plus deals per closing through the underwriting funnel), negotiating with sellers and brokers, structuring the debt and signing the loan (which on smaller deals or value-add bridges typically requires a personal recourse guarantee from the GP principal, and on agency loans involves narrow bad-boy carveouts that trigger only on specific bad acts like fraud or voluntary bankruptcy filing), conducting full due diligence on the property, underwriting the deal against actuals rather than broker pro formas, building the business plan, closing the transaction, hiring and managing the property management company, executing the value-add work, and reporting to LPs on a monthly or quarterly cadence through the hold.

The GP also handles every LP-facing operational task: subscription documents, accreditation verification under the appropriate Reg D offering, capital calls if needed, K-1 production and delivery (typically by mid-March each year), distribution scheduling, investor portal management, and the disposition or refinance process at the back end of the hold. The volume of work behind a well-run syndication is meaningfully greater than what most LPs assume from reading the quarterly update — the visible reporting is the surface of an operational discipline that runs continuously across the entire hold.

Limited Partner

The LP's role in a syndication is narrowly defined and intentionally passive. The LP evaluates the sponsor and the deal, signs subscription documents, wires capital, and then receives distributions and the K-1 according to the schedule disclosed in the offering. The LP has voting rights on a small set of major decisions (typically things like extending the hold beyond the projected period, changing the business plan materially, or replacing the property manager), but no day-to-day operational authority over the asset.

The asymmetry is deliberate: the LP is buying back time as much as they are buying real estate exposure. The structure exists so that the LP's worst-case downside in a normal scenario is loss of equity rather than ongoing operational liability, and so that the LP's contribution to the partnership ends once capital is wired. Distributions arrive monthly or quarterly depending on the deal, the K-1 arrives in March, and the LP's primary professional life continues uninterrupted.

Are real estate investments passive income?

Whether a real estate investment qualifies as genuinely passive income depends entirely on the structure of the ownership. Direct rental property ownership is not passive income in the operationally meaningful sense — even with a property manager handling tenant interactions, the owner is making capital expenditure decisions, signing for the debt, handling vacancy planning, and absorbing every operational risk that the property produces. Time investment is meaningful, particularly as the portfolio scales beyond one or two units.

Multifamily syndication as an LP, by contrast, is structurally passive. The GP signs the loan, hires the PM, makes the operational decisions, and reports back to the LP base. The LP receives recurring cash flow without any active management responsibility for the property. This structural distinction is the core of why multifamily syndication is one of the few real-estate ownership formats that genuinely produces what the IRS classifies as passive income — with all of the tax-treatment advantages (depreciation shelter, ability to offset other passive income, no self-employment tax on distributions) that passive income receives.

Free 5-Day Video Course

Everything you need to evaluate passive multifamily — in five short videos.

Five 7 a.m. emails over five mornings. Earned-vs-passive income, syndication mechanics, K-1 tax treatment, market cycles, and underwriting — no credit card, no sales pitch.

Get Instant Access →Free. Unsubscribe with one click.

Who can invest in an apartment syndication?

Eligibility to invest in a multifamily syndication is governed by SEC rules under Regulation D, which determine what kinds of investors a sponsor can legally accept into a given offering. The rules distinguish among three investor categories — accredited, sophisticated, and non-accredited — and the offering structure the sponsor selects (Rule 506(b) or Rule 506(c) of Reg D) determines which of those categories can participate. Understanding the distinction matters because it shapes who the sponsor can legally communicate with about a specific deal, and it shapes the verification documents an LP will be asked to provide before subscription.

1.) Accredited Investor Definition

An accredited investor under SEC Rule 501 of Regulation D is an individual (or joint household with a spouse) meeting at least one of the following financial thresholds: an annual income of $200,000 or more individually ($300,000 jointly) for each of the past two years, with a reasonable expectation of the same income in the current year, or a net worth exceeding $1 million excluding the value of the primary residence. The SEC also recognizes certain professional credentials (Series 7, 65, or 82 licenses) as alternate qualification paths.

The accredited threshold exists because the SEC's underlying view is that investors meeting the income or net-worth bar have the financial sophistication and the loss-absorption capacity to participate in private placements without the disclosure protections that public securities registration provides. Most LPs in multifamily syndication subscribe as accredited investors via the income or net-worth test — the SEC verification process for accredited status is straightforward and the offering structure (typically Rule 506(c) for advertised offerings or Rule 506(b) for relationship-based offerings) is built around accredited eligibility.

2.) Sophisticated Investor Definition

A sophisticated investor is a non-accredited individual who has sufficient knowledge and experience in financial and business matters to evaluate the merits and risks of a private placement, even though they do not meet the financial thresholds for accredited status. The sophisticated investor category exists in the Reg D framework specifically because Rule 506(b) offerings allow sponsors to accept up to 35 sophisticated investors alongside an unlimited number of accredited investors in the same offering, provided the sponsor takes reasonable steps to determine that each sophisticated investor genuinely meets the knowledge-and-experience standard.

In practice, sophisticated-investor subscriptions require more documentation than accredited subscriptions because the sponsor needs to establish the basis for the investor's qualification (typically through a detailed investor questionnaire covering investment experience, financial education, and prior private-placement participation). Sponsors who run primarily 506(c) offerings, where general solicitation is allowed and all investors must be verified accredited, do not accept sophisticated-investor subscriptions at all.

3.) Non-Accredited Investor Definition

A non-accredited investor is an individual who meets neither the accredited investor financial thresholds nor the sophisticated investor knowledge-and-experience standard. Non-accredited investors cannot participate in Rule 506(b) or Rule 506(c) offerings under Regulation D, which means non-accredited individuals are functionally excluded from most institutional-quality multifamily syndication deals. Other regulatory exemptions (Regulation A+, Regulation CF, intrastate offerings) permit non-accredited participation in specific structures, but the deal economics, sponsor quality, and operational discipline available in those structures are generally not comparable to the institutional multifamily syndication universe.

Multifamily syndication offerings

The offering structure a sponsor selects for a given deal depends on the capital raise size, the investor base the sponsor is targeting, and whether the sponsor intends to publicly advertise the offering. Real estate syndications are presented to LPs as an “offering” registered with the SEC under one of several exemptions from the full securities-registration requirements. The two exemptions that account for nearly all institutional multifamily syndication activity are Rule 506(b) and Rule 506(c) of Regulation D, and the distinction between the two is meaningful both for the sponsor (what they can advertise) and for the LP (what verification they will be asked to provide).

Reg. D; 506 (b)

Rule 506(b) is the relationship-based offering structure. Under 506(b), a sponsor may raise an unlimited amount of capital from an unlimited number of accredited investors plus up to 35 sophisticated investors per offering, but the sponsor is prohibited from any general solicitation about the specific deal. In practice this means a sponsor running a 506(b) raise cannot publicly advertise the offering — no blog posts naming the deal, no social media campaigns, no email blasts to anyone the sponsor does not have a pre-existing substantive relationship with. The investor list the sponsor raises from must consist of LPs who have an existing relationship with the sponsor that predates the specific offering.

The trade-off for the relationship constraint is procedural ease on the verification side: 506(b) offerings allow LPs to self-certify accredited status via the subscription documents, without the additional third-party verification documentation that 506(c) offerings require. Most established multifamily sponsors run a meaningful portion of their offerings under 506(b) because the relationship-based investor list they have built over time satisfies the no-general-solicitation requirement organically.

Reg. D; 506 (c)

Rule 506(c) is the publicly-advertised offering structure. Under 506(c), a sponsor may raise an unlimited amount of capital from an unlimited number of accredited investors (no sophisticated-investor allowance), and the sponsor is permitted to publicly advertise the specific offering — on the firm's website, through paid marketing, on social media, in newsletter campaigns, and through any other public channel. The trade-off is verification: every investor in a 506(c) offering must be verified as accredited through third-party documentation (CPA letter, attorney letter, brokerage-statement review, or third-party verification service), not merely self-certified.

506(c) offerings are operationally heavier on the front end because of the verification requirement, but they let sponsors expand the LP base beyond their existing relationship list. Sponsors choose between 506(b) and 506(c) deal-by-deal based on the raise size, the existing investor list capacity, and whether they want to add new accredited investors to the platform through public marketing of a specific deal.

How can I invest in a passive real estate investment like a multifamily syndication?

The mechanical path into a multifamily syndication starts with sponsor selection. The LP identifies the sponsor (typically through educational content, referrals, LinkedIn, or organic search — multifamily syndication is a relationship business, and the credible deals route through the sponsor's investor list rather than through public crowdfunding aggregators, which we walk through in our guide to how to find real estate syndication deals), joins the sponsor's investor list, completes accreditation verification, reviews specific deals as they are offered, and subscribes to the ones that match the LP's portfolio objectives.

Capital can be wired into a syndication from several sources depending on the LP's situation. The most common is direct personal capital wired from a brokerage or bank account. The second most common is capital held in a self-directed retirement account — a self-directed IRA (SDIRA) or solo 401(k), which allows the account owner to direct the account custodian to invest in alternative assets including private real estate syndications. We cover the SDIRA mechanics in depth in our guide to how to invest in multifamily real estate with a self-directed IRA. A Traditional IRA produces tax-deferred growth (contributions are tax-deductible, withdrawals in retirement are taxed at the prevailing rate), while a Roth IRA produces tax-free growth (contributions are not deductible, but withdrawals in retirement including all appreciation are tax-free). For SDIRA-funded multifamily investments specifically, the depreciation pass-through does not flow through to the account holder's personal taxes — the account itself owns the LP interest — which makes SDIRA capital especially efficient for syndication investments where the post-tax personal yield differential matters less.

Syndication vs. REIT

The structural difference between a multifamily syndication and a public REIT is direct ownership. A REIT is a publicly-traded company that owns income-producing real estate, and the investor in a REIT owns shares of the company's stock — they do not own any specific property and do not receive any of the property-level tax treatment that direct ownership produces. A syndication LP, by contrast, is a member of an LLC that holds a specific property, receives a K-1 with property-level depreciation pass-through, and shares in the specific outcome of that specific deal.

Seven dimensions separate the two structures in ways that materially affect LP outcomes: direct ownership (syndication yes, REIT no), tax benefits (syndication passes through depreciation, REIT distributes ordinary dividends that the investor pays full marginal rates on), diversification (REIT spreads across many properties automatically, syndication is concentrated in one property), barriers to entry (REIT shares trade for tens of dollars, syndication minimums typically run $50,000–$100,000), liquidity (REIT shares sell same-day, syndication LP interests are illiquid for the full hold), investment minimums (REIT shares as small as one share, syndication checks measured in tens of thousands), and value volatility (REIT shares move with the public equity market and trade at meaningful premiums or discounts to underlying NAV, syndication valuations move with the underlying property's NOI).

The syndication's most meaningful structural advantage over a REIT is the depreciation pass-through that produces the post-tax yield differential we walk through in the next section. The trade-offs are concentration risk (one property instead of dozens) and illiquidity (5- to 7-year hold instead of same-day liquidity), which are real costs that an LP should size appropriately against the after-tax yield advantage.

Syndication vs the stock market

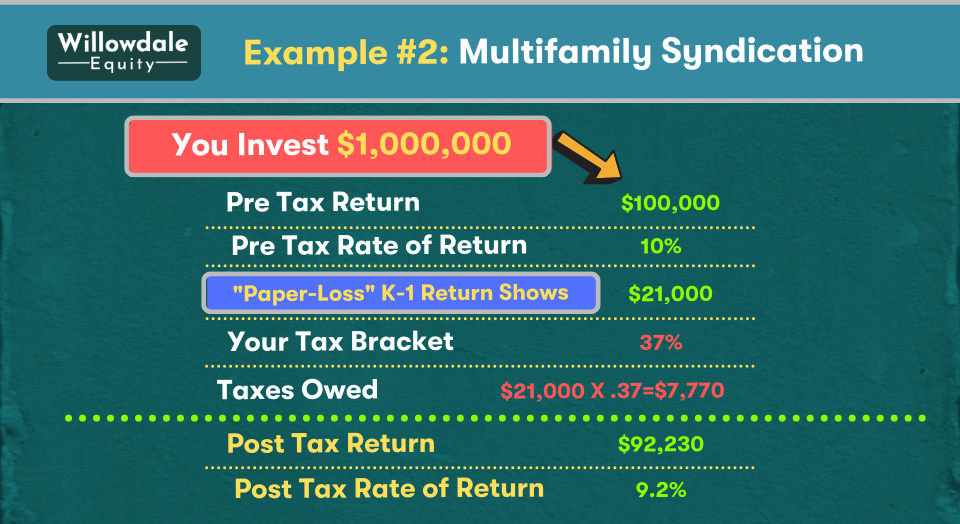

The most direct way to see the post-tax economics of a syndication LP position compared to direct stock market exposure is to work the same dollar amount through both with the same pre-tax return assumption. Both produce a 10% headline return; the after-tax outcomes diverge meaningfully because of the depreciation pass-through that syndication produces.

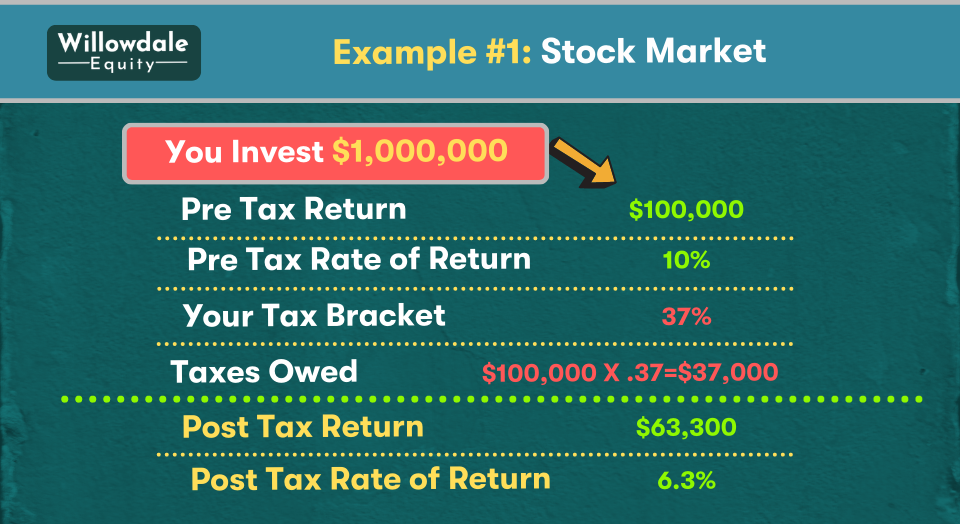

Example 1: The LP invests $1 million in the stock market and earns a 10% return for the year, or $100,000. The full $100,000 is taxed at the LP's marginal income tax rate — assume 37% for a high-income professional. Tax owed is $37,000, net to the LP after tax is $63,000, post-tax yield is 6.3%.

Example 2: The LP invests the same $1 million in a multifamily syndication and receives $100,000 in distributions during the year. Because the LP is a direct LLC member with pass-through depreciation, the K-1 shows net rental income of only $21,000 (the $100,000 in distributions minus $79,000 of allocated depreciation). At the same 37% marginal rate, tax owed is only $7,770, net to the LP after tax is $92,230, post-tax yield is 9.2%.

Same headline 10% return, materially different after-tax outcomes — nearly 290 basis points of post-tax yield differential in favor of the syndication. The mechanic that creates the gap is structural to direct real estate ownership and cannot be replicated through a public REIT or through any other equity-market vehicle, which is the core reason sophisticated LPs allocate to direct private real estate when they want post-tax yield rather than just headline return. The stock market position retains the advantage on liquidity and on diversification across many positions, which is why most LPs hold both rather than choosing one exclusively.

The behavioral dimension matters too. We have heard the same line repeated by prospects through every correction window: “I'm done with the stock market.” That sentiment is not investment advice, but it does point to a real underlying difference in how the two asset classes feel to own through volatility. Multifamily distributions do not disappear because the S&P is down 20%, and that operational reality matters meaningfully to a 50- or 55-year-old accredited investor whose retirement planning depends on durable income rather than mark-to-market account values.

Why real estate is the best passive income?

The strongest case for real estate as a passive income allocation is the combination of three properties that no other widely-available asset class offers in the same structure: durable cash flow that does not collapse in correction windows, pass-through depreciation that shelters the cash distributions from current tax, and equity growth through both forced appreciation (operator-driven NOI expansion) and amortization (mechanical principal paydown converting debt to equity each month). Public equities produce dividends but lose the depreciation shelter; bonds produce interest income at full marginal rates with no equity upside; REITs produce dividends but lose the direct-ownership tax treatment. Multifamily syndication is one of the few structures that holds all three properties simultaneously.

The structural reason this combination is available in real estate but not in most other private alternatives is the IRS tax treatment of direct real estate ownership specifically — depreciation as a non-cash expense, 1031 exchanges as a way to defer gain on disposition, cost segregation as a way to accelerate depreciation through the early years of a hold. These features are not loopholes; they are deliberate policy designed to encourage private capital flow into housing supply. The LP captures the policy benefit through the syndication structure.

The Yield Brief · Free Weekly Newsletter

Multifamily markets, rates, and policy — for accredited investors. 2k+ subscribers.

How do you get into passive real estate?

The practical path into passive real estate investing for most accredited investors begins with education, then sponsor selection, then deal-by-deal evaluation. The educational phase is what builds the framework for evaluating sponsors and deals critically — understanding the capital stack, the waterfall mechanics, the tax pass-through, the cycle considerations, and the structural differences between syndication and the alternatives an LP might otherwise consider (REITs, direct ownership, public real estate ETFs). Most LPs who get into trouble in their first syndication did so because they shortcut the educational phase and subscribed to a deal evaluated on superficial signals (projected IRR, marketing polish, social proof) without the underlying mechanics to ask the right questions of the sponsor.

If you are at the start of that educational phase, our free 5-Day Passive Real Estate Investing Mini-Course walks through the core LP-onboarding framework over five short emails — earned versus passive income, syndication mechanics, K-1 tax treatment, market cycles, and underwriting basics. From there, sponsor selection becomes a focused process: identify 5 to 10 sponsors with strong full-cycle track records in your target asset class, get onto their investor lists, read their market commentary and attend their webinars for several months before evaluating a specific deal, and then run sponsor diligence first and deal diligence second when an offering lands.

The 3 ways we build equity and add value to an apartment community

Equity in a multifamily property grows through three mechanisms that operate independently but compound when they all run at once. The first is forced appreciation, which is the operator-driven NOI expansion that comes from executing the value-add business plan — rent increases, expense compression, additional income drivers, operational tightening. The second is market appreciation, which is the cap rate compression or organic rent growth driven by market conditions outside the operator's control. The third is amortization, which is the mechanical principal paydown on the senior loan that converts debt into equity each month on the balance sheet.

The arithmetic is straightforward: multifamily property value equals net operating income divided by the prevailing market cap rate, so any operator-driven NOI expansion converts into equity at the cap-rate multiple (a $100,000 NOI lift at a 7% cap rate creates about $1.43 million of new property value, which after debt produces a corresponding equity expansion for the partnership). The sections below walk through each mechanic in turn.

1.) Forced Appreciation

Forced appreciation is the operator-driven NOI expansion that comes from executing the value-add business plan on the property after closing. The work splits into revenue-side initiatives (raising in-place rents to market through unit renovations and turn discipline, adding ancillary income drivers like utility billback programs, washer/dryer add-ons, parking fees, pet fees, and other-income line items) and expense-side initiatives (tightening operating expenses, renegotiating service contracts, leaning out the management overhead, improving collection rates through better tenant screening).

Both sides convert into property value at the prevailing cap rate. At our 69-unit Mill Gardens property, the water billback program alone — $30 per month on one-bedroom units, $35 on two-bedroom and larger — added roughly $2,250 in monthly NOI once fully adopted across the rent roll. At a 7% cap rate, that single operating initiative created roughly $385,000 of property value. The broader value-add story at the property moved average in-place rent from $516 pre-acquisition to $825 post-stabilization — a 60% rent lift — through a combination of unit renovations, tighter screening that improved the collection rate from 88% to 95%, and the operational discipline that comes with switching from a seller-self-managed property to a professional third-party management company.

One of the cleanest forced-appreciation wins at the same property was structural rather than cosmetic: the prior owner had been using a 1-bedroom unit as the leasing office, which removed it from the rent roll. We bought a 10×24 ADA-compliant modular leasing office, branded it, and placed it on previously unused green space at the property entrance, bringing the converted unit back online as the 69th rentable unit. That single decision added roughly $590 in NOI per month, or $7,080 per year — about $101,000 of value created from one structural change at the same 7% cap rate.

2.) Market Appreciation

Market appreciation is the share of equity growth that comes from market conditions outside the operator's direct control: cap rate compression that lifts valuations across the submarket, rent growth driven by employment and population growth in the metro, demographic trends that expand the renter pool. Operators can position to capture market appreciation through disciplined market selection on the front end — underwriting deals only in MSAs that screen well on population growth, employment growth and diversification, landlord-friendly regulatory environment, and supply/demand pipeline math — but the appreciation itself is exogenous to operator action.

Cycle stage matters here. Market appreciation runs strongest in Expansion phases of the real estate cycle (rising occupancy, accelerating rent growth, limited new supply) and slows or reverses in Hypersupply phases (new deliveries outpacing absorption, concessions reappearing, rent growth softening). Underwriting to a target market that is still in Expansion gives the operator the wind at their back; underwriting into a Hypersupply market means the value-add work has to fight the market's natural drift. We discuss cycle positioning in detail in our guide to the four phases of the real estate cycle.

3.) Amortization

Amortization is the principal-paydown component of equity growth, which is mechanical and continuous through the hold. Each monthly loan payment includes both interest and principal, and the principal portion reduces the outstanding loan balance dollar-for-dollar — which means partnership equity grows by exactly that principal-paydown amount each month, regardless of whether the property's NOI is expanding or its market value is appreciating. Over a 5- to 7-year hold, accumulated amortization on a typical agency loan with a 30-year amortization schedule converts a meaningful percentage of the original debt into equity.

Amortization is realized at the liquidity event — either at refinance (where the LP shares in the equity that was built through paydown on the existing loan) or at the eventual sale (where amortization-driven equity is monetized in full alongside the forced and market appreciation components).

The 4 types of multifamily real estate investing strategies

Multifamily syndication deals are typically categorized into one of four investment-strategy buckets that describe the property's risk profile, the operator's intended business plan, and the expected return distribution. Understanding the four categories helps LPs evaluate whether a specific deal matches their portfolio objectives before they read the underlying underwriting. The four categories run along a single risk-return continuum: Core (lowest risk, lowest expected return), Core Plus (slightly higher), Value-Add (the sweet spot for most accredited LPs seeking real return without taking development-level risk), and Opportunistic (highest risk, widest return distribution including the possibility of meaningful capital loss).

1.) Core Multifamily Real Estate Investments

Core multifamily investments are stabilized Class A properties in primary or strong secondary markets, typically less than 10 years old, with high occupancy at acquisition, minimal capital expenditure needed, and a long-duration hold thesis focused on income preservation and modest appreciation. The risk profile is conservative; the return expectation is correspondingly modest, typically in the high-single-digit IRR range. Core deals are most appropriate for capital preservation strategies and for LPs whose primary objective is current income with minimal volatility, rather than aggressive total-return targeting.

2.) Core Plus Multifamily Real Estate Investments

Core Plus investments are Class A or upper-Class B properties, typically 10 to 20 years old, that combine stable cash flow at acquisition with a light value-add business plan — some unit renovations, modest other-income initiatives, and operational tightening to push NOI without a full reposition. The risk profile is low to moderate; the return expectation is moderate, typically in the low-double-digit IRR range. Core Plus is the strategy that splits the difference between income-only Core and the heavier execution risk of Value-Add.

3.) Value-Add Multifamily Real Estate Investments

Value-Add multifamily investments are Class B or Class C properties, typically 30 to 40 years old, with meaningful operational and physical upside that the operator captures through the value-add business plan: unit interior renovations, exterior and common-area upgrades, operational tightening, additional income drivers, and a property-management replacement if the seller was self-managing. The risk profile is moderate to high; the return expectation is meaningfully higher than Core or Core Plus, typically in the mid-to-upper-teens IRR range when executed competently.

Value-Add is the strategy that produces the strongest risk-adjusted outcomes for most accredited LPs because the operator-driven NOI expansion is what creates the meaningful upside — the property is typically stabilized at 85–90% occupancy on acquisition (not a development-risk repositioning), the value-add work is well-understood operationally, and the eventual exit benefits from both the NOI lift and the cap-rate compression that comes with moving the property up a quality tier (Class C+ to Class B-, for example). At Willowdale, our core thesis is built around Value-Add multifamily acquisitions in Sun Belt markets that screen well on the 6-factor market screen.

4.) Opportunistic Multifamily Real Estate Investments

Opportunistic multifamily investments are the highest-risk category and include ground-up development, heavy reposition of distressed assets, adaptive reuse (converting office or hotel to multifamily, for example), and other situations where the underlying business plan involves meaningful execution risk that the operator must navigate to produce any positive return. The risk profile is high; the return expectation reflects that risk with wide outcome variability — the right opportunistic deals produce returns that exceed Value-Add, but the wrong ones produce meaningful capital loss for LPs.

Opportunistic exposure is appropriate for accredited LPs with diversified syndication portfolios who can absorb the loss of an opportunistic position without compromising the overall portfolio. Most LPs are better served concentrating their syndication exposure in Value-Add, which captures most of the upside available in private multifamily without the development-grade execution risk.

Frequently Asked Questions About Passive Real Estate Investing

Is passive income from real estate taxable?›

Yes, but the structural tax treatment of multifamily syndication income is meaningfully different from earned income or public-equity dividend income. The number that determines the LP's tax bill is the net rental income or loss reported in Box 2 of the K-1 (the partnership tax form delivered by mid-March each year), which is computed after the property's depreciation has been applied as a non-cash expense. In many years, the depreciation pass-through exceeds the LP's share of net cash flow, which produces a net taxable loss on the K-1 even when the LP received meaningful cash distributions during the year. Losses can be carried forward against future passive income from real estate. We cover the K-1 mechanics in depth in our guide to how the K-1 works in private real estate investing.

How do you get into passive real estate?›

The practical path starts with sponsor selection. Identify 5 to 10 sponsors with strong full-cycle track records in your target asset class, get onto their investor lists, read their market commentary for several months to build familiarity with how each sponsor thinks and reports, and then evaluate a specific deal when one lands. The discovery channel matters — most credible multifamily syndication deals route through the sponsor's investor list, through referrals from existing LPs, and through professional networks like LinkedIn, not through public crowdfunding aggregators (which tend to surface deals that did not subscribe out through the relationship channel). At Willowdale, we accept select accredited LPs into our private multifamily investment offerings; the first step is the free 5-day mini-course or a 1:1 introductory call.

How many properties do you need for passive income?›

One LP position in a multifamily syndication is enough to begin generating passive income from real estate, but the meaningful question is how much capital is deployed, not how many positions. A $50,000 LP check at an 8% preferred return produces $4,000 a year in current income; a $250,000 check at the same pref produces $20,000 a year, plus eventual share of any refinance or sale proceeds. Most accredited LPs build a portfolio across 3 to 5 sponsor relationships and 5 to 10 deals over a decade rather than concentrating in a single position, which spreads concentration risk across multiple properties and markets while preserving the operating discipline of working with sponsors the LP knows well.

What is an example of multifamily housing?›

Multifamily housing refers to any residential property structure that contains five or more separate dwelling units under one ownership and one tax parcel. The institutional multifamily syndication market focuses on apartment communities ranging from roughly 75 to 500+ units, typically configured as garden-style (multi-building, 2- to 3-story structures), mid-rise (4- to 6-story buildings), or high-rise depending on the market. A typical Willowdale acquisition example would be a 200-unit garden-style community in a Sun Belt MSA: roughly 200 individual residences, a mix of one-, two-, and three-bedroom floor plans, an on-site leasing office, amenities like a pool and fitness center, and a single ownership entity (the syndication LLC) holding the entire property under one mortgage.

How do multi family homes make money?›

Multifamily properties generate revenue across two main categories. The first is rental income from each unit, which is the dominant revenue line and scales with occupancy times average rent. The second is ancillary income from fees and services attached to the property: pet fees, parking fees, application fees, move-in fees, late fees, utility billback programs (commonly called RUBS), washer/dryer add-ons, and other line items that the operator can capture from the existing tenant base without additional capital expenditure. Larger properties can also generate non-tenant revenue from third parties — advertising panels, telecommunication antenna leases on rooftops, vending machines — though these are typically secondary contributors. Operating expenses (property management, payroll, utilities, repairs, insurance, real estate taxes) are subtracted from total revenue to compute net operating income (NOI), and NOI minus debt service produces the cash flow available for distribution to LPs.

Getting Started With Passive Real Estate Multifamily

Passive investing in multifamily real estate is one of the few structures available to accredited investors that simultaneously delivers durable cash flow, pass-through depreciation that shelters that cash flow from current tax, leverage that amplifies LP returns within a fixed-rate non-recourse debt envelope, and equity growth through three independent compounding mechanisms across a typical 5- to 7-year hold. The trade-offs are real — illiquidity for the full hold, concentration risk in specific deals, and dependence on the sponsor's execution — and they are why sponsor selection is the most important decision an LP makes.

The first step into the structure for most accredited investors is education. The framework for evaluating sponsors and deals critically is what separates LPs who do well across multiple deals from LPs who get into trouble on a single one. Our free 5-Day Passive Real Estate Investing Mini-Course walks through the LP-onboarding framework over five short emails covering earned-vs-passive income, syndication mechanics, K-1 tax treatment, market cycles, and underwriting basics. From there, the sponsor-selection and deal-evaluation work begins — for most LPs, it is the start of a multi-decade relationship with the asset class rather than a single transaction. At Willowdale, our work as multifamily operators across the Sun Belt is structured to give passive LPs access to institutional-quality value-add multifamily deals with the operational discipline and reporting transparency that the structure deserves.

Sources:

- Forbes, “If You Want To Know The Real Rate Of Inflation, Don’t Bother With The CPI“

- BLS.GOV, “Consumer Price Index data quality: how accurate is the U.S. CPI?“

- Investor.GOV, “Accredited Investors“

- IRS.GOV, “Partner’s Instructions for Schedule K-1 (Form 1065) (2021)“

- IRS.GOV, “Schedule K-1 (Form 1065)“

- FRED.StLouisFED.ORG, “Inflation, consumer prices for the United States“

- IPropetyManagment, “Average Rent by Year“

- HUFFPost, “The Six Things Non-Accredited Investors Need to Know About Title 111 of the JOBS Act“

- Bench.CO, “Schedule K-1 Tax Form: What It Is and When To Complete It“

- TheRealEstateCPA, “What is a Schedule K-1 Form?“

- Investopedia, “Stimulus Package“

- Investopedia, “Limitations of the Consumer Price Index (CPI)“

- Investopedia, “How Rental Property Depreciation Works“

- Investopedia, “What Is a 1031 Exchange? Know the Rules“

- Investopedia, “Crowdfunding for Non-Accredited Investors“

- Investopedia, “The Great Recession’s Impact on the Housing Market“

- Investopedia, “Does Inflation Favor Lenders or Borrowers?“

Next Step

Want to invest in the next one?

First-look access to upcoming Class B & C value-add multifamily acquisitions, before materials go out.

Apply Now →

Daniel Di Cerbo

Daniel is the Co-Founder and Principal of Willowdale Equity, a private real estate investment firm specializing in Class B & C value-add multifamily assets across the Southeastern U.S. He has been a sponsor on over $150M of multifamily acquisitions across Georgia and Texas.

Willowdale Equity content follows strict guidelines for editorial accuracy and integrity. Learn more about our editorial guidelines.